The AI Boom and the Dot-Com Bubble: Similar Psychology, Different Balance Sheets

July 19, 2026

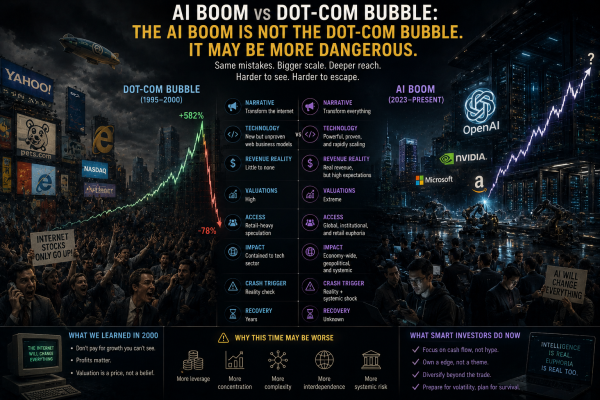

The easiest comparison between today’s AI boom and the dot-com bubble focuses on valuation, with many concluding that the current cycle is fundamentally safer because leading AI companies trade at far lower earnings multiples than technology stocks did in the late 1990s. At the peak of the dot-com era, countless businesses commanded triple-digit price-to-earnings ratios despite producing little cash flow, whereas today’s leaders, including NVIDIA, Microsoft and Oracle, generate enormous profits, maintain fortress balance sheets and trade at valuations that appear far more defensible on the surface.

That comparison is technically correct, but it misses the point because bubbles have never been defined by valuation alone. They emerge when psychology, capital allocation and rising asset prices reinforce one another until expectations begin expanding faster than the returns those investments can realistically produce. By that measure, the comparison with the late 1990s becomes far more compelling.

The Psychology Is Different. The Behaviour Is Not.

The dot-com bubble was driven largely by speculation attached to businesses with little economic substance. Investors financed companies built on ambitious projections, weak business models and little more than the promise that the internet would eventually transform the economy. Today’s AI leaders stand on much firmer foundations. They generate extraordinary free cash flow, dominate critical technology infrastructure and possess the financial strength to invest at a scale that few corporations in history could match.

That distinction matters because it changes the psychology of the cycle. Investors are no longer buying stories divorced from reality; they are buying exceptional businesses participating in what is almost certainly one of the most important technological shifts in decades. The technology is real, the productivity gains are increasingly measurable and AI will almost certainly reshape large sections of the global economy.

None of that, however, prevents capital markets from overshooting. Throughout history, revolutionary technologies have repeatedly attracted more capital than near-term returns could justify, not because the underlying innovation failed, but because investor expectations expanded faster than the economics supporting them.

The Reflexive Capital Cycle

The greatest risk in the current AI cycle is not fraudulent businesses or imaginary revenues but a self-reinforcing investment loop in which spending validates more spending.

Hyperscalers purchase enormous quantities of AI chips, allowing semiconductor companies to report exceptional growth and cash generation. Those profits finance additional infrastructure, while venture capital channels billions into AI start-ups that consume cloud services, encouraging cloud providers to accelerate investment still further. Enterprise software companies increase AI spending largely because competitors are doing the same, private capital subsidises adoption, rising equity valuations reduce the cost of capital and cheaper capital finances another round of expansion.

The cycle feeds upon itself. Rising investment produces rising revenues, rising revenues reinforce optimistic expectations and those expectations justify even greater investment. Nothing about this process is fraudulent, yet it remains inherently reflexive because current spending increasingly validates the assumptions that encourage future spending.

The Rise of Defensive Capital Expenditure

An equally important feature of the current cycle is that much of today’s AI investment appears defensive rather than purely economic. Large corporations increasingly believe they cannot afford to underinvest because the cost of falling behind may ultimately prove greater than the cost of temporary overinvestment. As a result, executives are deploying capital before monetisation models have fully matured, reasoning that infrastructure can be justified later if competitive positioning is secured today.

This creates what might best be described as FOMO capital expenditure, where investment decisions are driven less by demonstrated returns than by the fear of strategic irrelevance.

The closest historical parallel is arguably not the dot-com bubble itself but the fibre-optic boom that accompanied it. The internet unquestionably transformed the global economy, yet telecommunications companies built far more infrastructure than near-term demand required. The infrastructure eventually became indispensable, but many investors suffered devastating losses because capital arrived years before sustainable returns. Technological success and investment success are related and they are not identical.

A second, less discussed risk lies in the pace of technological improvement itself. If model performance continues advancing while the cost of training and inference declines faster than expected, the economics underpinning today’s unprecedented infrastructure buildout could begin to change. More efficient models require less compute, less energy and potentially fewer high-end accelerators to deliver comparable or even superior performance, weakening the assumption that current levels of AI capital expenditure will ultimately generate the returns implied by today’s valuations. That possibility does not undermine AI as a transformative technology. On the contrary, it may accelerate adoption by making advanced models dramatically cheaper to deploy. What it does challenge is the belief that every dollar being invested today will earn the economic returns investors currently expect, reinforcing a pattern seen throughout history where capital allocation overshoots even as the underlying technology succeeds.

A Stronger Ecosystem Can Produce a Longer Cycle

The current AI ecosystem is also structurally stronger than the internet bubble because a handful of extraordinarily profitable companies effectively finance much of the industry’s expansion. Rather than depending primarily upon speculative capital, today’s ecosystem is supported by businesses generating hundreds of billions of dollars in operating cash flow, allowing them to fund infrastructure, subsidise adoption, invest aggressively in research and nurture entire developer ecosystems without immediate concern for short-term profitability.

Paradoxically, that financial strength may extend the cycle rather than eliminate its risks. Strong balance sheets make optimistic assumptions more difficult to challenge because exceptional earnings provide genuine evidence supporting continued investment, allowing enthusiasm to compound for longer than it otherwise might. The result is a cycle that appears more stable than previous bubbles even as expectations continue drifting further ahead of long-term economic reality.

Where the Risk Actually Lies

The greatest risk facing investors is not that AI fails but that expectations eventually collide with the slower mathematics of mature markets. As infrastructure spending normalises, enterprise adoption becomes less explosive and competitive pressures compress pricing, revenue growth will inevitably moderate even if the underlying businesses remain exceptionally profitable.

That transition has historically been enough to trigger substantial multiple compression because markets value accelerating growth very differently from stable growth. Investors often assume that transformational technologies guarantee transformational returns, yet history repeatedly demonstrates that exceptional businesses can experience prolonged drawdowns once future optimism has already been incorporated into current prices.

The railroads transformed transportation, radio reshaped communication, the internet revolutionised commerce and smartphones permanently altered modern life, yet investors in each revolution experienced periods when outstanding companies lost half their market value simply because expectations had become detached from achievable returns.

Durability Is Not Immunity

None of this suggests that the AI boom is approaching immediate collapse. If anything, the financial strength of today’s dominant firms makes the cycle considerably more durable than the late-1990s technology bubble because genuine earnings, real cash generation and widespread commercial adoption provide a far stronger foundation than speculative internet start-ups ever possessed.

Durability, however, should never be confused with immunity. Markets rarely punish revolutionary technologies; they punish expectations that outrun the economic returns those technologies can deliver within a realistic timeframe. The current AI cycle appears less like a replay of the dot-com bubble than its more sophisticated successor, supported by real businesses, real infrastructure and genuine productivity gains, yet still governed by the oldest law in financial markets: expectations almost always expand further than sustainable returns.

That is the paradox investors repeatedly overlook. The technology can exceed every expectation, reshape the global economy and generate extraordinary long-term value while many investors still earn disappointing returns because they paid too much for certainty before the future had time to arrive.