Forecasting Is a Career Tool, Not a Market Tool

July 26, 2026

Why Most Forecasts Protect Reputation, Not Capital

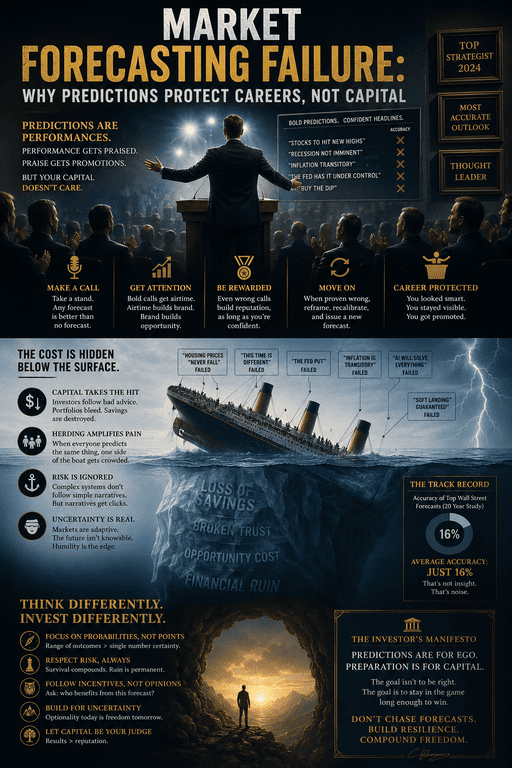

Financial markets are saturated with forecasts, yet their primary function is rarely to improve investment decisions. Instead, they protect reputations. Most forecasts are carefully constructed to appear thoughtful, balanced and adaptable, allowing the forecaster to remain credible regardless of the outcome. Accuracy is desirable but not essential. Survivability is.

This is not necessarily dishonest. It is the natural consequence of incentives. Investment strategists, economists and market commentators are judged less on whether they consistently predict the future than on whether they remain professionally credible after being wrong. Bold predictions create career risk, while moderate, highly qualified opinions are difficult to falsify. Over time, forecasting evolves into an exercise in reputation management rather than capital allocation, rewarding those who minimise personal risk rather than those who maximise analytical accuracy.

Consensus Is a Product of Human Psychology

Forecasting also reflects a deeper psychological reality. Human beings are social learners who instinctively seek safety in agreement, particularly during periods of uncertainty. As volatility rises, independent thinking becomes increasingly uncomfortable because being wrong alone carries a far greater emotional and professional cost than being wrong with everyone else. Consensus therefore expands precisely when uncertainty is greatest, not because the future has become clearer, but because the psychological cost of disagreement has become too high.

This is one of the recurring geometries of financial markets. As expectations converge, positioning converges with them, gradually reducing the diversity of opinion that allows markets to absorb new information efficiently. Agreement creates the illusion of stability while simultaneously making the system more fragile because an increasing amount of capital becomes dependent upon the same assumptions remaining true. The crowd mistakes consensus for certainty, when in reality consensus often marks the point where alternative outcomes are least appreciated.

Forecasts Arrive After the Opportunity

From a market perspective, forecasts rarely provide meaningful edge because they typically describe trends that prices have already discounted. By the time economists agree that growth is accelerating or strategists become confident about an emerging bull market, expectations have usually adjusted long before the reports are published. Forecasts therefore explain what has already happened more effectively than they anticipate what comes next.

Markets do not reward the obvious. They reward the gap between expectations and reality. Once a narrative becomes widely accepted, the opportunity increasingly shifts from analysing the prevailing story to identifying the assumptions embedded within it. The critical question is no longer whether the consensus is reasonable but whether expectations have become too dependent upon it remaining correct.

Forecasts Distort Time

Perhaps the greatest weakness of forecasting is that it encourages investors to think about destinations rather than journeys. A strategist may correctly predict that the market will finish the year higher, yet that prediction provides little protection if the path includes a thirty percent drawdown that forces leveraged investors to liquidate or causes institutions to rebalance risk. Markets rarely travel in straight lines because expectations expand and contract continuously, producing periods of euphoria, exhaustion and panic long before the final destination becomes apparent.

Capital is rarely destroyed because the long-term forecast proves incorrect. It is destroyed because investors underestimate the path required to reach it. Forecasts encourage patience when adaptation is required and conviction when flexibility would be more valuable, replacing observation with commitment at precisely the moments when changing conditions demand the opposite.

Structure Matters More Than Opinion

Experienced operators therefore pay far less attention to forecasts than to market structure because structure reveals how participants are behaving rather than what they claim to believe. Capital flows, liquidity, positioning, volatility and breadth provide direct evidence of changing conditions, whereas forecasts merely describe opinions about those conditions.

The questions that matter are therefore behavioural rather than predictive. Who is forced to act if volatility doubles? Where does liquidity disappear first? Which investors become sellers if prices move sideways rather than higher? How concentrated has positioning become around a single narrative? These questions expose pressure points within the system, allowing investors to identify fragility before it becomes visible in prices.

Markets rarely break because everyone is pessimistic. They break because too many participants have organised their capital around the same optimistic assumptions, leaving few buyers available once those assumptions begin to weaken.

The Geometry of Belief

Every forecast is ultimately a statement about belief, yet markets move not when beliefs are confirmed but when they fail. Prices adjust as expectations change, not as reality unfolds, which is why seemingly positive news can trigger declines while disappointing news occasionally sparks powerful rallies. The market is constantly measuring the distance between what investors expected and what actually occurred, rewarding surprise rather than certainty.

This is why forecasting repeatedly disappoints. It attempts to predict outcomes while largely ignoring the geometry of expectations that determines how markets respond to those outcomes. The future itself is rarely the decisive variable. The relationship between expectation and reality is.

The Real Edge

The most valuable skill in markets is therefore not forecasting but recognising when collective belief has become unstable. Once expectations become one-sided, markets require very little new information to produce outsized reactions because the adjustment comes from positioning rather than fundamentals. Mass psychology consistently reaches its greatest extremes when confidence appears strongest, creating periods where the consensus feels safest just as systemic fragility quietly reaches its peak.

Forecasts struggle in these environments because they are designed to survive criticism rather than volatility. Markets, however, care nothing for reputations. They respond only to the interaction between capital, expectations and behaviour, rewarding those who observe changing structures rather than those who defend yesterday’s predictions.