Foreign Investment in US Stocks: Altitude, the 1970s Echo, and What Happens When the Dollar Bends

Oct 30, 2025

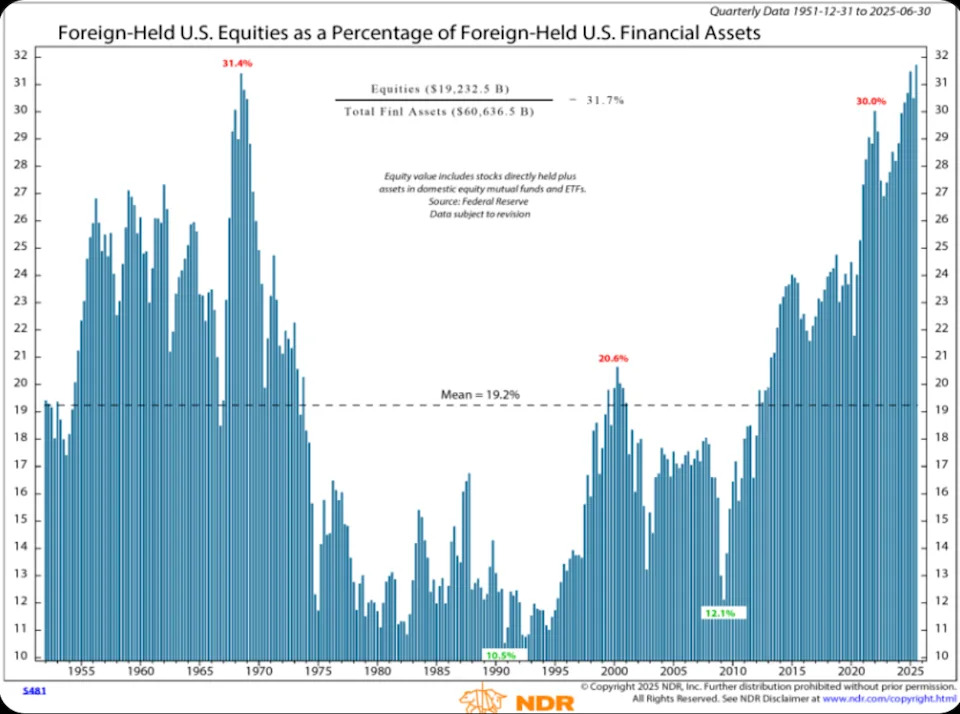

There are charts that shout, and charts that whisper. This one whispers altitude. Foreign investment in US stocks sits near ~30–31% of foreign-held financial assets—levels seen only twice in modern history, 1972 and 2000. The seven-decade mean is ~19.2%. Peaks at this height don’t predict doom; they change probability. They say the air is thin, the room is crowded, and the exit is narrower than it looks.

Source: https://finance.yahoo.com/

Mirror Altitude: When Price Outruns Pacing

From 1965 to 1972, US equities drifted higher while inflation doubled, deficits swelled, and war spending mounted. The S&P 500 climbed ~50% as costs thickened beneath the tape. Today’s rhyme is uncomfortable: stretched valuations, narrative dominance, and cash flow trailing price. The top seven names control roughly a third of the index by weight, an echo of the Nifty Fifty’s concentration. Foreign allocators have followed momentum into the same summit. That’s the comfort. That’s the risk.

Liquidity vs Conviction

Liquidity sculpts the statue, valuation is the marble. In the late 1960s, expanding money supply amplified the bid; today, large fiscal outlays and swollen balance sheets play the same accelerant. Rising prices validate the allocation, which draws in more flows, which lifts price—until the terrain under the story changes. Liquidity is merciful on the way up and clinical on the way down. Foreign investment in US stocks has been a momentum trade by another name.

Stagflation wasn’t born; it accreted. Credit restraint alternated with fiscal push, leaving policy at war with itself. Present day isn’t copy-paste, but the direction rhymes: deficits near ~6% of GDP, core services inflation sticky in the 4–5% range, the Federal Reserve leaning against price persistence while Congress leans into spending. Crosswinds don’t break a trend by themselves; they roughen it. They slow the time to next high and hasten the time to next doubt.

Currency as Battlefield

In 1971, convertibility snapped; within two years the dollar fell ~23%. Foreign investors didn’t wait for earnings to roll—they de-risked because currency had already stolen their return. Today the DXY sits near cycle highs, but peaks of this size are usually bends, not plateaus. If the dollar turns, foreign allocations can unwind faster than profits adjust. Foreign investment in US stocks lives and dies in FX: a 10% dollar slide can erase a year of “outperformance” when measured in the home currency of the allocator.

Three-Beat Pattern: Compression, Adjustment, Reversal

When altitude meets inflation pressure, history tends to keep time in three beats. First, valuation compression: multiples fall before earnings do. In the 1970s, P/Es marched from regal to middling while reported profits still looked respectable on paper. Second, earnings adjustment: input costs and wage stickiness tighten margins; from 1973–74, S&P earnings fell ~15%. Third, flow reversal: foreign equity exposure mean-reverts and can overshoot; in the 1970s, foreign shares of US financial assets slid from ~31% to ~10–12%. Patterns aren’t laws, but they’re not accidents either.

The toolkit is different now. The Fed has QE, forward guidance, standing repo, swap lines, emergency windows. These slow dislocations, backstop funding, and sedate panic spirals. They do not repeal valuation mathematics. They cannot force a Dutch or Korean pension fund to hold through a dollar drawdown. Airbags soften impact; they don’t move walls.

Tripwires: When to Expect the Bend

You don’t need to guess tops; you need to notice turns. Three simple tripwires: a 7–10% decline in DXY from a clear cycle high within six months; a breadth rollover where new highs narrow while indices still rise; and a 50 bps widening in high-yield spreads versus 20-day averages. One tripwire is noise. Two are a caution flag. Three are regime change. When those trip, the probability of mean-reversion in foreign investment in US stocks rises—and speed, not slope, does the damage.

State Over Story: Receipts from the Tape

We don’t preach without receipts. On 7 May, a rare “Mother of All Buy” trigger fired—built for moments when emotion outruns logic. From that day, the S&P 500 advanced roughly 12%, the Nasdaq 100 more than 15%, and the Composite over 16%—evidence that process can outlast hysteria in the USA tape . In April, the VIX spiked and then faded; fear flashed, never caught, no true top-level euphoria; pullbacks were buys because the crowd wasn’t manic while the trend was up . The lesson is portable: read state, not story; trade rules, not headlines. The same discipline applies to foreign flow risk—wait for the tripwires, then act.

Baseline, Stress, Stabilisation

Baseline (Mean Reversion): foreign equity share drifts from ~30% toward the ~19% long-run mean over 12–24 months. Multiples compress more than earnings; currency contributes part of the move. Positioning: trim US mega-cap concentration into narrowing breadth; add to cashflow-heavy defensives, energy, and selective ex-US cyclicals if the dollar bends.

Stress: a dollar bend arrives alongside margin pressure—unit labour costs up, interest expense as share of sales rising, energy friction. Foreign outflows accelerate, rhyming with 1973–74. Allocations test 10–12% troughs. Positioning: bigger underweight in cap-weight US; add USD-hedged ex-US exposure; favour balance-sheet strength and short duration cash flows.

Stabilisation: liquidity support, fiscal coordination, and moderating inflation flatten the descent. Multiples compress, but flow unwind is paced, not panicked. Positioning: rotate, don’t rage—reduce concentration, keep dry powder for pattern breaks, avoid binary bets.

We filter regime trades through five instruments that ignore narrative and describe state. Breadth: are equal-weight indices confirming or is cap-weight doing all the lifting? Credit: are spreads tightening (healing) or widening (strain)? Real yields and USD: direction and pace, not levels; rising real yields with a firm dollar compress duration. Volatility term structure: is the curve inverted into “good news” (fragile) or re-steepening into “bad news” (digesting)? Leadership: do cyclicals and quality carry on red days, or has the market narrowed to one theme? Three aligned signals justify action; otherwise—wait. Waiting is a position.

Regional and Structure Friction

Flows are not monolithic. Europe, Japan, the Middle East, and Asia ex-Japan don’t share the same currency base, risk budget, or mandate language. A French insurer sees a stronger USD as a gift; a Korean fund sees it as a tax. Structure matters too: sovereign wealth funds can move swiftly; insurers are slower; retail ETFs move fastest and panic fastest. Expect the unwind to begin at the edges—ETF de-risking on FX pain—then move inward as boards read the same charts we’re discussing today.

Portfolio Playbook: Practical Moves

Trim into narrowing breadth and rising concentration. Cap single-theme exposure. Scale out; don’t lunge. Pair a modest cap-weight underweight with quality defensives and energy that benefit from re-pricing of risk and a weaker USD. Build a watchlist of ex-US cyclicals to add if DXY rolls—buy strength where currency turns a headwind into a tailwind. Keep your USD hedges flexible; treat them as risk throttles, not religion. Stage entries and exits; price pays you for discipline.

What the Fed Can and Cannot Do

Swap lines can calm funding. Standing repo can ease collateral stress. QE can compress term premia. None of these force the hands of foreign committees who see their home-currency P&L bleeding. Foreign investment in US stocks responds to currency first, valuation second, story last. The Fed controls one of those three for a while; the other two return on their own timetable.

The Final Loop: Altitude Isn’t Neutral

The chart doesn’t scream “crash.” It whispers “altitude.” Altitude sets the script. At 31% against a 19% mean, you need uninterrupted liquidity, narrative control, and dollar strength to hold this height. If any of those falter, flows reverse—theatre rules apply: people walk to the exit in on the way in; they run on the way out. Airbags soften impact; they don’t suspend gravity.

So prepare the playbook now, while the room is calm. Watch DXY for the bend, breadth for the roll, credit for the leak. When two trip, you lighten. When three trip, you move. Foreign investment in US stocks got you here on story; getting out will require reading state. That’s how you keep the gains when the music shifts key.

Flashes of Brilliance That Shift Perspectives