Why We Use Options for Structure, Not Speculation

Jul 27, 2026

We receive questions about options whenever markets become slower, more volatile or directionless. The assumption is usually the same: if stocks are no longer producing easy gains, perhaps options offer a faster route to higher returns. That assumption explains why so many investors eventually lose money with options. They approach them as instruments of leverage when they should be viewed as tools for improving structure.

That difference is fundamental. We rarely emphasise options because managing multiple contracts across dozens of positions quickly becomes operationally demanding, and most investors are better served by keeping their portfolios simple. Simplicity is an underrated advantage. Complexity often creates the illusion of sophistication while quietly increasing the number of decisions capable of producing mistakes.

When we do use options, however, the objective is remarkably straightforward. We are not attempting to predict the next short-term market move. We are improving how capital enters and exits positions we already want to own.

Time Becomes an Ally Instead of an Enemy

Most investors unknowingly position themselves against time. They buy options hoping a stock will move quickly before time decay steadily erodes the value of their position. Their success therefore depends on being correct about both direction and timing, a combination that dramatically lowers the probability of consistent success.

Selling options reverses that relationship: Instead of paying for time, you collect payment from those willing to speculate on it. Instead of requiring immediate movement, patience itself begins generating income. That subtle shift changes the psychology of investing because urgency gives way to discipline. Rather than chasing price, you allow price to come to you. Time, which normally works against speculators, begins working alongside disciplined investors.

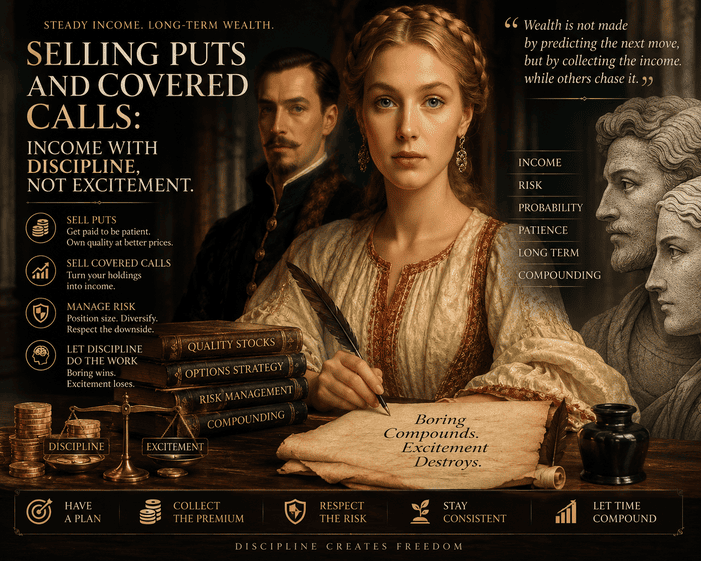

Cash-Secured Puts: Being Paid to Accumulate

Selling cash-secured puts is best understood as placing a limit order that compensates you while you wait. Every contract represents one hundred shares, meaning the cash required for assignment should already be available. The objective is not to avoid owning the stock but to establish ownership on terms you find attractive.

If the shares decline to your chosen strike price, assignment occurs and your effective purchase price is reduced by the premium already collected. If the shares remain above the strike, the option expires and you retain the premium without purchasing the stock.

Either outcome can represent success because both were acceptable before the trade was entered. This is important as it separates investing from speculation. The investor asks, “Would I be happy owning this company at this valuation?” The speculator asks, “Can I avoid assignment?” One seeks ownership. The other seeks excitement.

Covered Calls: Structuring the Exit

Covered calls apply the same philosophy in reverse. Instead of waiting to accumulate, you are establishing conditions under which you are prepared to reduce or exit an existing position.

By selling a call against shares already owned, you immediately receive premium income that increases your effective selling price. Should the shares rise above the strike price, they are called away at a valuation you previously considered acceptable. Should they remain below the strike, you retain both the shares and the premium, allowing the process to be repeated.

Covered calls therefore work particularly well when positions approach fair value or when markets begin moving sideways after substantial advances. Rather than demanding continuous price appreciation, the portfolio continues generating returns even during periods of limited movement.

The Crowd Buys Excitement. Professionals Sell Probability

One of the more revealing differences between professional and retail behaviour lies in how options are typically used. Retail investors are naturally attracted to buying options because leverage promises extraordinary gains from relatively small amounts of capital. Unfortunately, leverage also magnifies the effects of poor timing, emotional decision-making and unrealistic expectations. The attraction lies in the possibility of exceptional returns, while the mathematics quietly work against the majority of participants.

Professional investors frequently approach the market from the opposite direction. They recognise that consistent wealth is usually built through probabilities rather than predictions. Selling carefully selected options on companies they already wish to own or are willing to sell transforms uncertainty into income while allowing time decay to become an additional source of return rather than a persistent obstacle.

This is less exciting than buying lottery-ticket options, but it is also considerably safer and easily repeatable.

Structure Matters More Than Premium

The greatest mistake investors make is allowing premium income to become the objective. Premium is merely compensation for accepting clearly defined obligations. Selling puts on companies you would never willingly own converts income into unnecessary risk. Selling covered calls on positions you are emotionally unwilling to part with guarantees disappointment whenever the shares continue climbing after assignment.

- The premium should never dictate the trade.

- The underlying business should.

- Everything else follows naturally from that decision.

Options as Behavioural Discipline

Viewed through the Tactical Investor framework, options are valuable because they reinforce disciplined behaviour rather than encourage emotional reactions. Cash-secured puts reward patience during periods of uncertainty. Covered calls encourage investors to define acceptable exit levels before greed begins influencing judgement. Both strategies shift attention away from predicting headlines and toward managing expectations, valuations and capital allocation. That is their real advantage as they introduce structure into decisions that investors too often make emotionally.

Used with quality businesses, sufficient cash reserves and realistic expectations, options become another way of improving portfolio discipline rather than another source of speculation. Used carelessly, they simply magnify the behavioural mistakes investors were already making in the underlying shares.

The objective has never been to maximise option premiums or to outsmart the market over the next few weeks. It is to build positions methodically, reduce the influence of emotion and allow probability, patience and disciplined execution to do what frantic prediction rarely can.