May 20, 2026

One thing investors need to separate clearly is the difference between a weak country and a mispriced equity market. Indonesia is not behaving like a collapsing frontier economy held together with tape and slogans. The macro data simply does not support that narrative. GDP growth remains resilient, the banking structure is relatively stable, downstream investment continues rising, and the country is becoming increasingly important in commodities, industrial processing, power systems, and regional manufacturing chains.

That matters because markets eventually reconnect with macro reality, though often much later than expected.

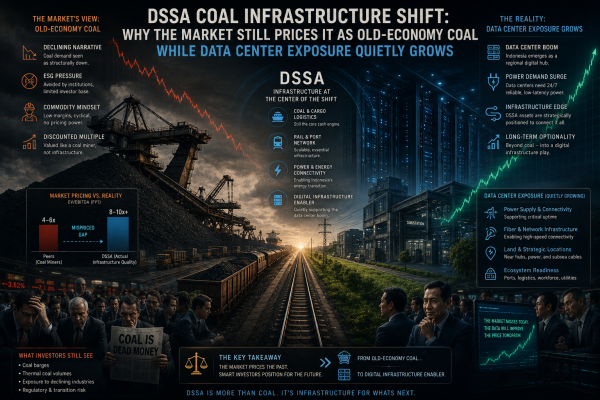

Why DSSA Is More Than a Coal Story

The frustration many investors feel with PT Dian Swastatika Sentosa Tbk comes from that disconnect. The company is not some broken shell running on fumes. It sits on substantial coal-linked cash flow, infrastructure exposure, power systems, digital infrastructure positioning, and growing relevance tied to connectivity and data-center demand. Yet the market continues to treat it largely as a politically inconvenient coal-linked old-economy name.

This is not unusual during transition phases.

Historical Parallels: Energy and Coal Reratings Investors Forget

History shows that commodity bull markets often begin with equities refusing to believe the move is sustainable. The same thing happened with energy producers during 2021 and 2022. Oil prices surged aggressively while many energy stocks lagged badly because institutional capital distrusted the durability of the cycle, ESG pressure distorted flows, and investors assumed another collapse was inevitable. Meanwhile many of those companies quietly accumulated enormous amounts of free cash flow before valuations finally rerated violently higher.

Coal producers across Asia experienced similar treatment after COVID. Prices surged, cash flow exploded, yet many operators traded at absurdly low multiples because global capital had already mentally classified coal as a dead industry. The market preferred narratives over balance sheets. That works for a while, until the cash accumulation becomes impossible to ignore.

DSSA increasingly looks like a variation of that same setup.

What the Market Is Actually Discounting About DSSA Stock

The market appears to be discounting conglomerate complexity, ownership structure, valuation opacity, liquidity mechanics, and fears around future commodity normalization far more aggressively than actual solvency or strategic positioning. In simpler terms, the market is still looking backward while parts of the company are already evolving forward.

That distinction matters.

The Coal-to-Data-Center Transition the Crowd Hasn’t Noticed

The crowd still mentally files DSSA under “coal,” while the business itself increasingly intersects with power infrastructure, connectivity systems, digital infrastructure, and data-center relevance. Markets often recognize those transitions late because investors anchor themselves to the original narrative long after the underlying structure begins changing.

This is where mass psychology matters more than spreadsheets alone.

How Mass Psychology Distorts Hard-Asset Pricing

Markets are not perfectly efficient pricing machines. They are liquidity and psychology systems operating together. Capital crowds into fashionable narratives while neglecting areas associated with older cycles, even when those older sectors continue generating real cash flow and strategic relevance. For years technology narratives absorbed enormous flows while many hard-asset businesses traded as if physical systems no longer mattered. Yet the world still runs on electricity, minerals, fuel, logistics, and infrastructure. Digital systems sit on top of physical systems, not outside them.

Why Commodity Reratings Happen Violently, Not Gradually

The interesting part is that commodity and infrastructure reratings rarely happen gradually once sentiment finally shifts. The market usually ignores hard assets for too long, then suddenly realizes supply is constrained, cash flow remains real, and strategic relevance never disappeared in the first place. At that stage valuations often adjust violently rather than smoothly.

The Risks Investors Should Still Take Seriously

That does not mean DSSA is risk free. No serious investor should pretend otherwise. Commodity-linked businesses remain cyclical, ownership structures matter, liquidity can distort pricing for extended periods, and emerging-market equities often remain disconnected from fundamentals longer than investors expect. But there is a meaningful difference between a structurally broken company and a company temporarily trapped inside an outdated narrative.

Right now DSSA increasingly appears closer to the second category.

| Investor Concern | Market’s Current Framing | What the Evidence Actually Suggests |

|---|---|---|

| Coal Exposure | Politically toxic, terminal industry | Still generating substantial cash flow |

| Conglomerate Complexity | Hard to model, avoid it | Hides emerging infrastructure value |

| Digital Infrastructure | Not part of the DSSA narrative | Quietly becoming strategically relevant |

| Liquidity Mechanics | Adds risk premium | Distorts price, not fundamentals |

| Commodity Normalization | Cash flow assumed to collapse | Supply tightness still intact |

Emerging Market Hard Assets vs AI Mega-Cap Concentration

The broader pattern also matters. Emerging-market hard assets remain relatively neglected while enormous amounts of global capital continue concentrating into AI mega-caps and short-duration certainty trades. That imbalance can persist for longer than seems rational, but historically it rarely persists forever if commodity strength survives, balance sheets remain healthy, and strategic relevance keeps expanding.

Eventually valuation gaps become too large to ignore.

The Pattern: Disbelief, Cash Accumulation, Then Sudden Rerating

Commodity bull markets often begin with disbelief. Then cash piles up quietly, supply tightens further, narratives weaken, and suddenly the rerating begins. By the time the crowd notices, much of the easy move has already happened.

The market tends to underprice physical systems right before scarcity becomes impossible to deny, especially when most capital is hypnotized by digital abstraction while forgetting what the digital world still depends on underneath.