May 19, 2026

Markets often struggle most with companies caught between two phases. They understand stable growth stories. They understand collapsing businesses. What they dislike are transition periods where the assets remain strong but the timing, execution, and sequencing become difficult to model.

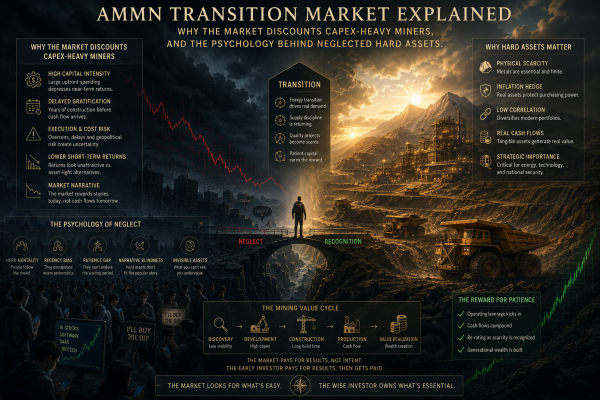

That is increasingly the situation surrounding PT Amman Mineral Internasional Tbk.

Why Indonesia’s Macro Strength Doesn’t Save AMMN Stock

The frustration around AMMN partly comes from the larger misunderstanding surrounding Indonesia itself. The country is not behaving like a fragile commodity appendage waiting to implode. Indonesia continues showing resilient GDP growth, strategic importance in global resource chains, rising downstream investment, improving industrial policy, and increasing relevance in energy-transition supply systems. The macro backdrop looks far healthier than many external narratives suggest.

But strong macro conditions do not automatically translate into smooth equity performance, especially during capital-intensive transition phases.

What the Market Is Really Pricing Into AMMN

AMMN is being discounted largely because the market sees giant capex digestion, smelter transition complexity, production sequencing concerns, and execution uncertainty. None of those issues imply the company is structurally broken. What the market is really saying is something much simpler: “the assets may be excellent, but the transition period could remain messy.”

That distinction matters because markets often punish uncertainty more aggressively than weakness itself.

Why Capital Avoids Transition-Phase Hard Assets in 2026

The current environment especially favors short-duration certainty. Capital remains heavily concentrated in mega-cap technology, AI infrastructure, and momentum-driven narratives where investors believe earnings visibility appears cleaner. Emerging-market hard assets, particularly those requiring long investment cycles and operational transitions, remain relatively neglected despite improving strategic importance.

This pattern is not unusual historically.

Historical Parallels: Gold Miners and Energy Producers

Gold miners experienced similar treatment during parts of the 2003–2005 and 2018–2019 cycles. Gold prices improved, yet many mining equities initially lagged because investors distrusted management execution, worried about cost inflation, feared dilution, or preferred direct exposure to bullion itself. Later, once confidence stabilized and cash flow proved durable, many miners rerated aggressively.

Energy producers during 2021–2022 followed a similar path. Oil prices surged while many equities remained discounted because investors assumed the strength would collapse quickly. Cash flow accumulated quietly before valuations finally adjusted upward.

AMMN sits inside that type of environment, though with a more complicated transition profile.

The Capex Digestion Problem and Modeling Complexity

Unlike simpler commodity operators, the company is navigating major capex phases and industrial processing transitions that temporarily cloud valuation visibility. Markets dislike complexity because complexity reduces confidence in near-term modeling. Institutional capital especially prefers businesses where future earnings can be forecast with relative simplicity. Once a company enters a major transition stage, investors begin discounting execution risk, timing risk, cost overruns, and sequencing uncertainty simultaneously.

That often compresses valuations even when long-term strategic value remains intact.

How Crowd Psychology Distorts Hard-Asset Pricing

The broader issue is that markets today remain heavily tilted toward immediate clarity and liquidity concentration. Capital crowds toward areas where narratives appear clean and familiar while ignoring sectors tied to physical systems, industrial infrastructure, and resource scarcity. Yet history repeatedly shows that hard assets become most valuable precisely when they are most neglected.

This is where psychology matters more than headlines.

Markets are not rational allocation machines operating perfectly from spreadsheet logic alone. They are crowd-behavior systems shaped by liquidity flows, fear, narrative concentration, and institutional positioning. At certain moments the crowd becomes so concentrated in fashionable sectors that large valuation distortions develop elsewhere.

Those distortions can persist for a long time.

But they rarely persist forever if the underlying assets remain strategically important and financially viable.

Transition Friction vs Structural Decline: The Critical Distinction

That does not mean every neglected commodity or industrial company suddenly becomes a great investment. Timing still matters. Execution still matters. Balance sheets still matter. AMMN’s transition phase cannot simply be dismissed because it introduces real uncertainty around sequencing and operational delivery.

Still, there is an important difference between a business facing temporary transition friction and a business facing structural decline.

| Characteristic | Transition Friction | Structural Decline |

|---|---|---|

| Asset Base | Remains strategically valuable | Eroding or obsolete |

| Cash Flow Direction | Temporarily compressed, recoverable | Permanently impaired |

| Capex Profile | Heavy now, productive later | Maintenance-only, no growth |

| Demand Trajectory | Long-term tailwind intact | Structurally fading |

| Market Treatment | Discounted on uncertainty | Discounted on deterioration |

Right now AMMN increasingly resembles a market struggling to price long-term strategic assets during a difficult intermediate phase rather than a company collapsing underneath its own weight.

The Commodity Cycle Pattern: Disbelief Before Rerating

Commodity cycles frequently begin with disbelief and transition confusion. The market first discounts the sector aggressively, assumes normalization will crush profitability, and avoids long-duration uncertainty. Then gradually supply tightens, infrastructure demand remains strong, cash flow stabilizes, and valuations rerate once investors realize the scarcity story never disappeared.

The crowd usually notices that shift late.

By then the easy part of the move is often already over.