What Is Velocity of Money: Manipulating Inflation Through Spending Speed

June 3, 2025

The question isn’t if the system will crack under this manipulation—it’s when. Be prepared. Stay calm. And above all, recognize that the velocity of money is not just a number; it’s a weapon wielded by those who benefit most from keeping the rest of us in the dark.

Introduction: The Sleepwalk Economy

You might suspect I’m about to take a turn into esoteric terrain—maybe invoke Gurdjieff and his 4th Way teachings about self-remembering. Fair enough. I am, but only to draw a line straight to market behaviour.

According to the Work, man is a machine. Not metaphorically. Literally. He reacts, he obeys impulses, he runs on loops. Until he becomes aware of it, he isn’t living—he’s just playing out a script. And in markets, most participants do exactly that. They read inflation headlines, listen to the Fed, and then respond in predictable, mechanical ways, like trained dogs chasing numbers.

But here’s the twist: Gurdjieff’s version of “self-remembering” isn’t about reflecting on the past. It’s about seeing yourself now—as you move, as you act, as you repeat. Translating that to the economy, it means recognising that inflation and the velocity of money are not mysteries. They’re mechanical. Programmed. Connected.

Yet somehow, the narrative continues to be distorted by the media, economists, and anyone with a stake in keeping the machine shrouded in fog. Because if you truly understood that velocity drives inflation, you’d know when the engine is about to redline. And right now? The RPMs are rising quietly, even as everyone pretends we’re cruising.

Inflation: A Symptom, Not the Disease

The Velocity of Money (VM) is a measure of how quickly money circulates in an economy. Technically, it’s calculated as the ratio of nominal GDP to the money supply. However, behind this sterile formula lies a powerful lever that governments and central banks have repeatedly used to manipulate inflation, manage public sentiment, and exert control over economic dynamics.

VM isn’t just an economic statistic—it’s a weapon. By accelerating or decelerating the speed of money’s movement, authorities create inflationary or deflationary forces that shape the market, often in ways that serve political goals rather than economic stability. Let’s break this down and expose how VM has been a tool of manipulation.

Inflation is commonly misunderstood as rising prices, but it is merely a symptom. The real disease is excessive money creation, often cloaked as “stimulus” or “relief.” For decades, this money never reached the hands of ordinary people. Instead, it sat in bank reserves, suppressing VM and keeping inflationary pressures at bay. This was the game post-2008: money printed for banks, not people.

COVID changed everything. Under the guise of necessity, the government put money directly into people’s hands—stimulus checks, unemployment benefits, and small-business loans. This wasn’t generosity; it was calculated. By injecting cash into the broader economy, VM accelerated, unleashing inflationary forces that policymakers could conveniently blame on “supply chain disruptions” or “global tensions.”

Post-COVID Tactics: Immigration and Government Expansion

With COVID programs winding down, new excuses were needed to keep money flowing. Enter illegal immigration and government hiring sprees. These weren’t accidents or lapses in border policy—they were deliberate moves to pump cash into the system.

Illegal immigrants were provided housing, food, and even cash stipends—direct injections that boost VM. Similarly, Biden-era policies to expand government hiring disguised as “infrastructure investments” or “inflation reduction” acts were just avenues to keep VM high. Every newly hired government worker becomes a cog in the inflationary machine, spending money that fuels rising prices.

What Happens if Velocity Falls?

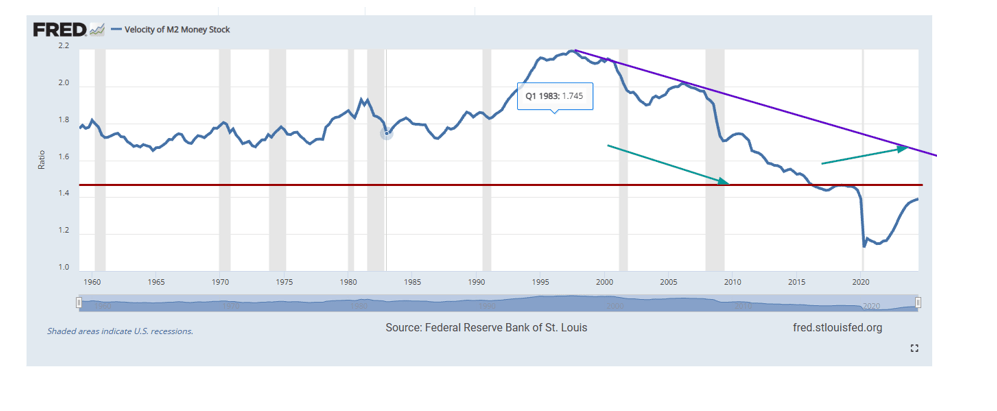

Now, imagine a scenario where VM slows. If policies like mass deportations or government workforce reductions were enacted, the system would face a deflationary threat. Deflationary forces, distinct from outright deflation, emerge when spending slows, reducing demand. Bond markets tend to thrive in such an environment, as lower volatility has historically aligned with falling bond yields and rising prices.

Yet, today’s bond markets defy this pattern. Despite soaring VM since COVID, bond yields remain volatile—a sign of deeper structural instability. Should VM revert to its historical mean, the system’s fragility could finally come to light.

Lessons from China: A New Playbook for VM

China has watched this manipulation with keen interest. Facing deflation, they’ve adopted the U.S. playbook, increasing salaries for government workers for the first time in years and funnelling money to small businesses. The logic is simple: if you want the value of VM to rise, give money to those who spend it, rather than hoard it.

This strategy reveals the core truth: VM is controlled by who receives the money. Billionaires and corporations don’t spend; they save or invest in ways that don’t circulate money through the economy. It’s the “average Joes” and small businesses that drive VM—and the government knows it.

Act Like a Machine, But Watch the System

You don’t need to remember you’re acting like a machine—you need to see it. In markets, awareness beats memory. Most investors are operating on autopilot, reacting to narratives rather than mechanisms. When it comes to inflation, they’re fed the usual distractions: energy prices, supply chains, war headlines. But those are noise. The real driver? Velocity of money (VM). And it’s not abstract—it’s engineered.

Inflation Wasn’t an Accident

The inflation we’ve lived through wasn’t a side effect of COVID. It was a carefully staged consequence. Central banks had been printing for years, but velocity stayed low—money sat in reserves, inflating asset bubbles but never touching the ground economy. No movement, no mass inflation.

Then came the stimulus era. Trillions were pushed directly into consumer hands. This wasn’t generosity. It was a controlled ignition. Velocity spiked. People spent. Prices climbed. And suddenly, inflation was back—but it wasn’t organic. It was manufactured.

Velocity: The Silent Trigger

Forget the CPI. Track VM. The higher it moves, the faster inflation follows. That’s the sequence. Government hiring, stimulus, and even immigration policy—all played roles in accelerating velocity. More cash flowed through the system, chasing the same goods. Demand surged, but it wasn’t natural—it was strategically induced.

Powell’s comment that “a little inflation wouldn’t be so bad” was never offhand. It was a signal. Inflation was the goal. VM was the lever.

The Hidden Cost of Control

This system doesn’t just respond to policy—it responds to intentional circulation. Expand government employment? VM rises. Offer benefits to undocumented immigrants? VM rises. These actions were disguised as compassion or recovery, but their function was the same: to keep money flowing and fuel the illusion of growth.

But velocity cuts both ways. Push it too far, and you risk hyperinflation. Pull it back too fast, and the machine stalls. Neither outcome is clean. But this isn’t about economics anymore. It’s about control—and the illusion of stability.

The Weapon No One Talks About

Velocity of money isn’t just a stat—it’s a control mechanism. When used well, it masks rot. When it slips, the mask comes off. We’re not seeing inflation because of demand. We’re seeing it because of intentional economic distortion. The media spins it. The Fed sells it. But underneath, it’s all velocity.

Understand that, and you’re no longer chasing the market—you’re tracking the architects. The real question isn’t what inflation is doing. It’s what velocity is being made to do—and why.