Market Liquidity Dies First. Panic Comes Later.

July 26, 2026

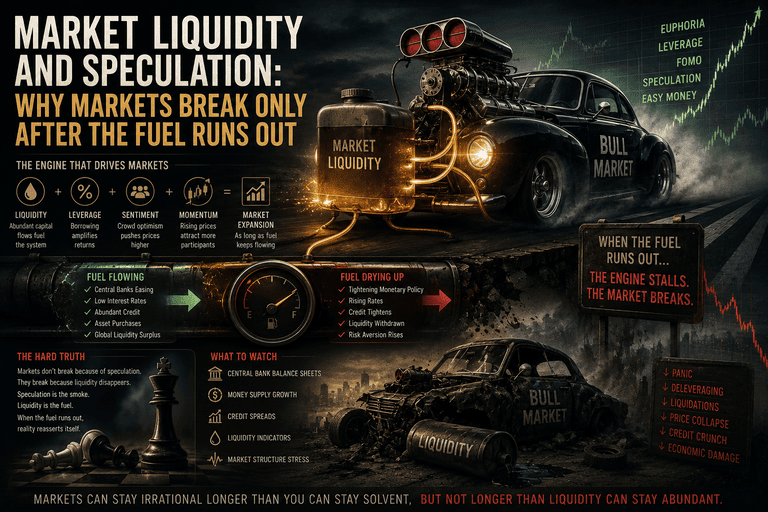

One of the most persistent myths in investing is that markets collapse because speculation becomes excessive. History suggests something far more subtle. Speculation rarely destroys a bull market on its own because optimism is not the fuel driving higher prices. Liquidity is. As long as capital remains abundant, borrowing costs remain manageable, and financial conditions continue accommodating risk-taking, investors can sustain valuations that appear detached from economic reality for far longer than logic would seem to allow.

The real danger emerges when the underlying source of that optimism begins weakening while speculative positioning remains elevated. Markets rarely collapse because investors suddenly become irrational. They collapse because the financial conditions supporting that irrationality begin deteriorating beneath the surface. By the time psychology finally changes, liquidity has often been tightening for months, leaving an increasingly leveraged system vulnerable to even relatively modest shocks.

The Primitive Isn’t Speculation. It’s Liquidity.

Speculation is not the driver of bull markets. It is the visible expression of abundant liquidity.

When money is readily available, financing is inexpensive, and credit expands easily, investors naturally become more willing to assume risk. Higher asset prices reinforce confidence, encouraging additional borrowing, which pushes prices even higher. Rising markets create the appearance that risk has diminished when, in reality, leverage is quietly increasing throughout the financial system. The optimism that dominates late-stage bull markets is therefore less a cause than a consequence of liquidity conditions that continue rewarding increasingly speculative behaviour.

This distinction explains why markets often ignore deteriorating fundamentals for extended periods. Investors focus on earnings, valuation and economic headlines, yet liquidity frequently overwhelms those variables until the financial system itself begins experiencing stress. The crowd mistakes rising prices for improving fundamentals when both are often being driven by the same underlying source: abundant liquidity.

Every Major Bubble Follows the Same Structural Geometry

Although every market cycle has unique characteristics, the underlying structure repeats with remarkable consistency. The Asian Financial Crisis and the collapse of Long-Term Capital Management in 1998 generated widespread fear and convinced many investors that the bull market had ended. Instead, policymakers restored liquidity, confidence quickly returned, and markets entered the most speculative phase of the dot-com bubble. The correction did not terminate the cycle. It strengthened it by removing weaker participants while leaving liquidity largely intact.

The years preceding the Global Financial Crisis displayed a similar pattern. Stress within housing and credit markets became visible well before the broader market collapsed. Financial institutions were already showing signs of strain during 2007, yet equity markets repeatedly recovered as liquidity continued supporting speculation. Only after funding conditions deteriorated sufficiently did confidence unravel rapidly, transforming isolated problems into a systemic crisis.

History demonstrates that valuation alone rarely ends speculative cycles. Liquidity determines how long those cycles survive, while leverage determines how violently they eventually unwind.

Liquidity Doesn’t Eliminate Risk. It Delays Recognition.

One reason investors repeatedly underestimate market cycles is that liquidity masks structural weakness. Capital continues flowing, financing remains available, and asset prices continue rising despite increasingly fragile foundations. As long as participants can refinance debt, borrow against appreciating assets and access abundant credit, the financial system appears remarkably resilient. The apparent stability encourages still greater risk-taking, reinforcing the belief that markets have entered a fundamentally different environment.

This creates one of investing’s most dangerous feedback loops. Strong performance attracts new capital. New capital supports higher valuations. Higher valuations justify additional leverage. Greater leverage produces even stronger returns during favourable conditions. The cycle becomes self-reinforcing until liquidity begins tightening faster than the system can comfortably absorb.

By that stage, the market is no longer merely optimistic. It has become dependent upon continued liquidity simply to maintain existing valuations.

Today’s Market Reflects Many Familiar Characteristics

The current environment exhibits several characteristics commonly associated with late-stage market cycles, although history never repeats with perfect symmetry. Equity markets have generated exceptionally strong gains, enthusiasm surrounding artificial intelligence continues attracting substantial capital, leadership remains concentrated among a relatively small group of companies, volatility remains subdued by historical standards and leverage throughout the financial system remains elevated. None of these developments independently guarantees a market reversal, but together they suggest a market increasingly reliant on favourable liquidity conditions.

At the same time, one important source of hidden support has largely disappeared. Over recent years, trillions of dollars parked within the Federal Reserve’s Reverse Repo Facility gradually flowed back into financial markets, quietly offsetting the effects of tighter monetary policy. That reservoir has now been largely exhausted, removing a source of liquidity that previously helped stabilise financial conditions beneath the surface.

Markets can certainly continue advancing despite this change. Aggressive fiscal spending, sustained corporate investment in artificial intelligence, continued foreign demand for U.S. Treasury securities or resilient private credit markets may all continue supporting liquidity longer than many investors expect. Nevertheless, the system becomes progressively more fragile when multiple sources of liquidity must continually offset rising borrowing requirements simply to preserve existing momentum.

The Transition From Optimism to Panic Happens Faster Than Most Investors Expect

Speculation rarely disappears gradually. Confidence often remains remarkably resilient until liquidity begins tightening in a meaningful way. Once financing conditions deteriorate, psychology changes with surprising speed because leverage amplifies every shift in sentiment. Investors comfortable holding risk during periods of abundant liquidity suddenly become anxious about preserving capital once borrowing becomes more expensive or funding less available.

Selling accelerates because declining liquidity reduces the market’s ability to absorb that selling. Borrowers become forced sellers. Margin calls trigger additional liquidation. Financing conditions tighten further as lenders become increasingly cautious. The very liquidity that previously supported rising asset prices begins disappearing precisely when demand for liquidity becomes greatest.

This sequence transforms what initially appears to be an ordinary correction into something considerably more dangerous. Panic is rarely the beginning of the process. It is usually the final stage of a deterioration that has already been unfolding quietly beneath the surface.

Why Investors Miss Both Extremes

Mass psychology consistently misinterprets both the beginning and the end of market cycles because it focuses on current emotions rather than changing liquidity conditions. During speculative peaks, investors convince themselves that liquidity will remain permanently abundant and that structural risks no longer matter. During market panics, those same investors assume deteriorating conditions will persist indefinitely, even as liquidity may already be beginning to stabilise beneath the surface.

Markets typically respond to changes in liquidity before public sentiment adjusts. Recoveries often begin while economic headlines remain overwhelmingly negative because financial conditions improve before confidence returns. Likewise, major declines often begin while optimism still dominates because liquidity weakens before psychology finally recognises the change.

The crowd therefore arrives late at both turning points. It embraces excessive optimism near market peaks and excessive pessimism near market bottoms, precisely because it mistakes prevailing emotion for underlying reality.

Fragility Is Not the Same as Imminent Collapse

One of the most important distinctions investors can make is understanding the difference between fragility and inevitability. A financially fragile system can continue producing impressive returns for extended periods provided liquidity remains sufficiently supportive. Indeed, some of history’s strongest rallies have occurred during the final stages of major bull markets, precisely because investors gradually abandon caution as rising prices reinforce confidence.

Today’s environment appears increasingly dependent upon multiple liquidity sources operating simultaneously. Inflation has already demonstrated its capacity to re-emerge, government deficits remain historically large despite relatively healthy economic conditions, Treasury issuance continues expanding, the Reverse Repo reservoir has largely disappeared and pockets of stress periodically appear within credit markets. None of these developments guarantees an immediate breakdown. Together, however, they reduce the system’s margin for error.

Fragility should therefore be understood as increasing sensitivity rather than certain collapse. The stronger the dependence upon continuous liquidity, the greater the potential consequences should that liquidity weaken unexpectedly.

Preparation Matters More Than Prediction

Investors frequently become consumed by predicting the precise timing of market crashes, yet history suggests that timing alone rarely determines long-term success. Many investors correctly identify structural weaknesses only to position themselves too early, while others ignore growing risks until conditions have already deteriorated beyond easy repair. Understanding liquidity provides a more useful framework because it shifts attention away from dramatic predictions and toward the evolving conditions that sustain or weaken market resilience.

Markets often resemble an overstretched rubber band. Tension accumulates gradually while prices continue rising, creating the illusion that the underlying structure remains healthy. Only when liquidity deteriorates sufficiently does leverage begin unwinding faster than financial markets can comfortably absorb, exposing weaknesses that had existed long before prices finally reflected them.

History continues delivering the same lesson in different forms. Speculation survives as long as liquidity continues feeding it, but once that fuel begins disappearing, psychology changes with extraordinary speed. Investors who understand that sequence spend less time trying to predict the exact day markets will reverse and more time recognising when the balance between liquidity, leverage and psychology is quietly shifting beneath the surface.

Beyond the Headlines