2020 COVID Stock Market Crash: Fear Fueled the Greatest Opportunity

August 31, 2025

This Wasn’t Just a Crash. It Was a Mass Psychological Break.

The 2020 COVID crash wasn’t a correction. It was a collective nervous breakdown dressed in red candles. Markets didn’t fall—they convulsed. Algorithms short-circuited. Humans froze. Commentators declared the financial system dead by Thursday. It was less an orderly sell-off and more a stampede through a burning theatre, with everyone clawing for the same exit.

And in that vacuum—while fear roared and reason vanished—opportunity screamed.

This isn’t a postmortem. It’s a decoding of crowd behaviour under existential pressure. When the world loses its bearings, markets speak the raw language of panic. The sharp don’t just endure it; they turn the screams into entry points.

High V-Readings Don’t Just Signal Volatility—They Expose Emotional Extremes

Forget the sanitised language of quant models. V-readings are not numbers; they’re heart rates. When VIX spikes into the stratosphere, it’s the market’s pulse hammering under stress. High V doesn’t just mean turbulence. It means pricing is distorted, perception is skewed, and the crowd is selling assets at terror discounts.

March 2020: 1,000-point mood swings in the Dow became routine. That wasn’t noise; that was emotional liquidity—fear-driven sellers on one side. High-conviction contrarians quietly accumulating on the other.

Then came the snap. A 3,600-point Dow rocket in three days. That wasn’t divine intervention. That was panic sellers running out of ammo and smart money stepping in with surgical precision. Similar surges appeared in 2008 after capitulation, and in 1987 after the bloodletting. Panic doesn’t end with calm. It ends with exhaustion.

Even now, when V is high but the trend is bending upward, fear still seeps from the edges. That’s the setup: emotional distortion + structural rebound = asymmetric opportunity.

“Back Up the Truck” Isn’t a Cliché. It’s a Tactical Command.

The “mother of all buy signals” didn’t arrive in a tailored suit. It came wrapped in blood-red headlines, empty shelves, and apocalyptic forecasts about “the end of capitalism.” Perfect.

When insiders start buying in the middle of a crisis, they’re not feeling brave—they’re executing informed conviction. During the March 2020 crash, insider buying surged to multi-year highs. CEOs and CFOs backed the truck. They knew that once the stampede burned itself out, valuations would snap back like a coiled spring. They were right. Amazon, Nvidia, and Apple didn’t just recover—they exploded to new highs while retail traders were still hiding under the table.

This is where panic and clarity part ways. The herd sees blood and runs. Strategic operators see blood and calculate.

“Back up the truck” doesn’t mean mindless buying. It means focusing on quality, value, and emotional pricing. It’s what Buffett did in 2008 with preferreds. It’s what disciplined funds did in 1987. It’s what the best did in 2020.

The Real Lesson: Stupidity Panics, Clarity Profits

Every crash has its chorus of doom. Every rebound rewards the clear-eyed. In 2020, retail panic drove Amazon’s stock price down to $1,700, while insiders quietly bought. By late 2021, it had surpassed $3,500. Nvidia cratered below $200, then tripled. Apple dipped 30 percent, then led the next leg of the bull market.

The crash wasn’t a tragedy. It was a transfer of wealth flowing from the hysterical to the focused, from those staring at headlines to those reading the balance sheets.

Next time the pulse spikes, remember: volatility isn’t a warning sign. It’s a starting gun.

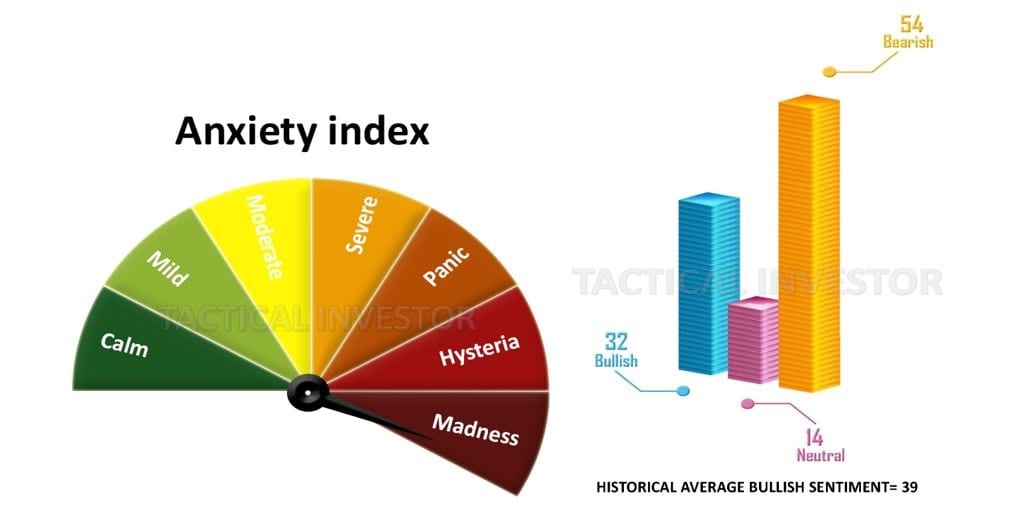

Three Weeks of Relentless Insider Buying

Insiders have been backing the truck up. Those with privileged information are exploiting this market decline to load up on shares. One of the cleanest ways to gauge the intensity is through the sell-to-buy ratio. A reading of 2.00 is neutral. Anything below 0.90 signals extreme optimism. The latest reading is 0.35. That isn’t buying. That’s a feeding frenzy.

Vickers’ standard NYSE/ASE One-Week Sell/Buy Ratio stands at 0.33, and the overall one-week reading is 0.35. This mirrors periods of aggressive insider accumulation during late December 2018 (Christmas Eve crash), early 2016 (mid-cycle correction), and the depths of late 2008 to early 2009. Every one of those moments turned out to be extraordinary buying opportunities for those who acted. Insiders are now broadcasting the same message again.

Insiders Are Buying Hand Over Fist

Corporate executives and officers are scooping up their own shares at the fastest pace in years. Sundial Capital Research reports insider sentiment at levels that historically precede strong equity performance. Historically, peak insider buying has correlated with a median 20% S&P 500 gain over the following year. Since 1997, the benchmark has posted 12.6% gains on average in the 12 months after robust insider accumulation.

Jason Goepfert of Sundial calls insider activity a positive signal—not a guarantee, but a sharp tell. Insiders don’t spend their own money aggressively if they expect a prolonged downturn.

Behavioural Breakdowns: What the 2020 Crash Exposed

Loss aversion ruled the tape. Investors weren’t trying to make money—they were trying not to feel pain. Neuroscience confirms loss activates the same brain regions as physical injury. When portfolios bled, logic left. Survival mode took the wheel.

Recency bias turned headlines into gospel. March 2020 was declared “unprecedented,” and investors promptly forgot 2008, 1987, and every panic before. All that existed was now, and in the now, the world was ending.

Crowd mimicry turned selling into synchronized panic. One hedge fund dumped, ten followed. Retail panicked. Twitter echoed. CNBC packaged it. Fear went viral. This wasn’t price discovery. It was emotion discovery.

1987 vs. 2020: Different Catalyst, Same Psychology

Black Monday 1987 was triggered by programmatic trading and panic feedback loops. One day. Down 22%. No virus. No lockdowns. Just human fragility under pressure.

2020 unfolded over weeks, global and drawn-out, but emotionally identical. In both cases, panic selling drove prices far below intrinsic value. Contrarians were mocked—then enriched. Rebounds came faster than almost anyone expected.

In 1987, Buffett quietly bargain-hunted while media mourned capitalism. In 2020, he bought Japanese trading houses while retail investors were hoarding Clorox and beans. Different backdrop. Same mistake.

Real-Time Contrarian Plays That Defied the Herd

Airlines and Energy: The mob screamed “never flying again.” A few studied history, saw the temporary nature of pandemics, and bought Delta and Exxon priced for extinction. Twelve months later, returns hit 80–100%.

REITs and Commercial Real Estate: Zoom became a religion. Office space was “dead.” Smart investors bought SL Green and Realty Income at 40–50% discounts to book. They bet on normalcy before it was fashionable.

Value over Growth: While the herd chased tech, the sharp money rotated early into industrials, cyclicals, and mid-cap value—right where nobody was looking.

The contrarians didn’t just bet against the crowd. They bet against emotional trauma—and won.

Market Crashes Are Recurring Psychological Algorithms

Crashes follow a script:

Shock → Panic → Capitulation → Opportunity → Regret

It’s a generational Groundhog Day. Boomers froze in 1987. Gen X in 2000. Millennials in 2008. Gen Z in 2020. Each swore they’d “buy the dip next time.” Each froze again when it came.

Volatility doesn’t paralyze. Mirrors do. People see their fear reflected back at them and fold. Those who break that loop don’t just survive—they build empires while everyone else is hyperventilating.

Crisis Is the Great Market Filter

Every few years, the market shakes the tree. The weak fall off. The strong climb higher. Strength isn’t in the charts—it’s in the mindset. Survivors of 2020 weren’t lucky stock pickers. They were psychologically antifragile. They welcomed chaos and understood a brutal truth: fear creates mispricing, and mispricing creates wealth—if you can stand in the fire without flinching.

Case Study: Buffett’s Apple Strike

While panic spread in 2020, Berkshire Hathaway increased its stake in Apple. Buffett wasn’t chasing headlines; he was exploiting them. While the herd dumped shares, he bet on cognitive distortion correcting itself. Apple rebounded sharply, turning a crisis into billions.

When the Herd Freezes, You Load

Volatility isn’t the enemy. It’s the test. When the VIX spikes and headlines scream:

- The crowd freezes.

- Pundits preach caution.

- Capital shifts from the emotional to the prepared.

This is the moment when wealth transfers hands. The only question is which side you stand on.

The Volatility Paradox: Weaponising Chaos

The 2020 crash wasn’t just a collapse—it was a mispricing festival for those who stayed calm. Volatility terrified the herd but enriched the few who turned into it. That’s the paradox: what scares the majority empowers the disciplined.

How the Bold Played the Storm

Volatility-Based Allocation: Adaptive traders adjusted exposure based on volatility signals, not price action. This kept drawdowns controlled and positioned them to reload near the bottom.

Options Tactics: With the VIX above 80, options became weapons. Long straddles and volatility arbitrage strategies exploded while equities melted.

Sector Rotation: Volatility didn’t hit evenly. Travel and hospitality bled; digital infrastructure and remote work surged. Zoom, DocuSign, and Nvidia became lifeboats while airlines sank.

Volatility ETFs: Traders who timed products like UVXY precisely walked away with 500%+ gains. These weren’t buy-and-hold plays—they were surgical strikes. Miss the window, miss the kill.

Volatility rewards skill, not hope.

Chaos Sorts Pretenders From Players

The 2020 crash exposed emotional mechanics, not just financial weakness. High volatility was a contrarian signal, not a warning siren. Insider buying surged while retail fled. Fear was loud; conviction was quiet.

Remember:

- High volatility often precedes major moves. Fear is camouflage, not prophecy.

- Insider buying at volatility peaks isn’t a coincidence—it’s calculated.

- Herd mimicry, recency bias, and loss aversion aren’t bugs; they are the system.

- Chaos isn’t noise. It’s the signal.

Volatility Is the Test, Not the Enemy

The 2020 crash proved once again that markets move when emotions misfire under stress. For the psychologically armed, that’s the moment of power. Every panic is a portal. Every selloff is a setup. Every volatility spike is a doorway most won’t walk through.

Those who don’t just survive the storm—they own the calm that follows.

Final Strike: Clarity Owns the Aftermath

The 2020 COVID crash was not a tragedy for everyone. It was a filter. Those who froze, chased headlines, or waited for “certainty” were harvested. Those who read the tape, trusted their preparation, and stepped in while fear blinded the crowd didn’t just recover—they multiplied. History has no sympathy for panic, only receipts. Buffett bought Apple. Insiders bought their own blood in the streets. Skilled volatility traders turned chaos into asymmetric windfalls. The herd told itself, “Next time.” The prepared acted.

Crashes don’t destroy wealth. Stupidity and hesitation do. Clarity under pressure decides who pays and who collects.

Expand Your Mind: A Selection of Intriguing Articles

Indoctrination: The Good, The Bad and the Ugly (Jan 15)