Uranium Price Forecast 2025: The \$47 Billion Supply Crisis Nobody Saw Coming

Updated Mar 17, 2026

The numbers don’t lie, but the market does. While Wall Street obsesses over AI stocks and crypto volatility, a \$47 billion supply crisis is building in plain sight. Uranium prices have surged 300% since 2020, yet 94% of institutional investors remain completely unpositioned for what’s coming next.

The brutal math: global uranium demand sits near 192 million pounds annually. Production stalls at 156 million. That’s a structural deficit widening every quarter. This isn’t a dip — it’s a compounding supply crisis that will either mint millionaires or destroy those arrogant enough to bet against physics.

The uranium price forecast for 2025 isn’t about chart patterns. It’s about the intersection of three unstoppable forces: exploding nuclear demand, constrained supply, and geopolitical weaponisation of energy infrastructure. The math is simple. The opportunity is massive. The window is closing.

Global Demand Surges: The Nuclear Renaissance Nobody Expected

Forget everything you think you know about nuclear power. While environmental activists spent decades demonising atomic energy, smart money quietly positioned for the biggest energy transition since oil replaced coal.

The demand data is staggering:

• China’s Nuclear Domination: 53 reactors under construction, targeting 150 total by 2030. Current capacity: 50 GW. Target: 200 GW by 2035. Each gigawatt requires roughly 200,000 pounds annually. China alone will consume 40 million additional pounds per year.

• Global Reactor Pipeline: 436 operational reactors worldwide, 65 under construction, 110 planned. The pipeline represents 35 million pounds of new annual demand by 2030.

• The ESG Reversal: \$2.8 trillion in ESG funds now recognise nuclear as essential for net-zero targets. BlackRock, Vanguard, and State Street — controlling \$20 trillion — reversed their nuclear stance in 2023. When the world’s largest money managers pivot, commodity prices follow.

• SMR Acceleration: 72 small modular reactor projects globally with 85 GW combined capacity. Unlike traditional reactors requiring 15-year construction timelines, SMRs deploy in 5–7 years. Demand spikes arrive faster than supply can respond.

The psychological shift is unmistakable. Nuclear went from pariah to saviour in 24 months. Germany is reconsidering its shutdown. Japan is restarting post-Fukushima reactors. Belgium extended reactor lifespans by 20 years. South Korea resumed expansion after a brief moratorium. This isn’t gradual adoption — it’s panic buying disguised as energy policy.

Supply Constraints: The Perfect Storm of Scarcity

While demand explodes, supply is trapped in a death spiral engineered by decades of underinvestment and geopolitical miscalculation.

• Production Deficit: Current: 36 million pounds annually. Projected 2025: 52 million pounds. Projected 2030: 89 million pounds. This isn’t a shortage — it’s a supply cliff.

• Mine Development Paralysis: Average time from discovery to production: 15–20 years. Development cost: \$1.5–3 billion per major mine. The pipeline is insufficient to meet even 2025 demand.

• Kazakhstan Concentration Risk: One country produces 43% of global uranium — 67 million pounds annually. Political instability, infrastructure limitations, and resource nationalism threaten the world’s largest supply source. That’s not diversification — it’s a single point of catastrophic failure.

• Enrichment Oligopoly: Russia controls 44% of global enrichment capacity. China controls 24%. Combined: 68%. US domestic enrichment: 4%. Enrichment facilities cost \$10–20 billion and take 15 years to build. Russia and China didn’t just corner the market — they built an economic chokehold on Western energy security.

• Inventory Depletion: Commercial reactor inventories have dropped 85% since 2010. Strategic reserves sit at 15-year lows while fuel requirements hit 15-year highs. When buffers disappear, price volatility explodes.

• Secondary Supply Collapse: Russian HEU weapons conversion — historically 10–15% of reactor feed — ended in 2013. That eliminated 15–20 million pounds of annual supply permanently.

• US Import Dependency: 99% of uranium concentrate is imported. Top sources: Canada (25%), Kazakhstan (22%), Australia (15%), Russia (14%). When domestic production covers 1% of consumption, you’re not an energy superpower — you’re a client state.

• The HALEU Crisis: Next-generation reactors require High-Assay Low Enriched Uranium (HALEU). Russia holds 100% of commercial HALEU production. US domestic capacity: zero until 2027 at earliest. Every advanced reactor project depends on Russian fuel until then.

• No Strategic Reserve: The US has no strategic uranium reserve despite 20% of electricity generation depending on nuclear. China maintains 10-year reserves. When supply shocks hit, China hoards while America scrambles.

Current global inventory: 18-month supply. Historical comfort level: 36 months. Time to replenish at current production rates: 8–12 years. The supply crisis isn’t theoretical — it’s mathematical certainty.

Policy Shifts and Strategic Initiatives

In 2024, President Trump signed executive orders targeting a fourfold increase in US nuclear capacity to 400 GW by 2050, streamlining regulatory processes and promoting SMR development. The Prohibiting Russian Uranium Imports Act bans enriched uranium imports from Russia, with waivers in place until 2028 for supply chain adjustment. Both moves underscore the urgency to develop domestic enrichment and diversify sources.

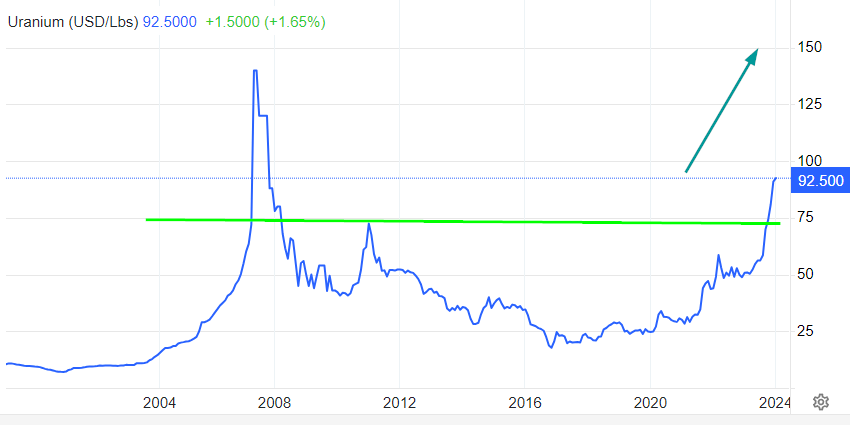

When Price Meets Precision: The Uranium Forecast Revisited

Source: www.tradingeconomics.com

As of Nov 19, 2023, Uranium is crafting a visually compelling and robust pattern, breaking through all previous resistance zones. The pivotal factor hinges on achieving a monthly close above 75, preferably 78, unlocking the path to 141 and beyond, marking a series of new all-time highs. Astute investors should welcome and embrace sharp pullbacks, recognising them as strategic entry points to capitalise on market sentiment and potential opportunities. Tactical Investor Update Nov 19, 2023

Uranium is showing a solid and impressive trend. It has broken through previous resistance levels and is now setting the stage for new record highs. What’s important now? Uranium needed to close above 75 to 78 every month, and the higher the close, the better the long-term outcome. It culminated the month at 81, surpassing hidden resistance pivot points and further strengthening the long-term bullish case. Uranium has now paved the way for a move to the 141 and a series of new record all-time highs. Market Update Dec 3, 2023 (sent out to subscribers)

Market Dynamics: The \$65 Basement vs. \$80 Term Price Divergence

The technical signals are screaming, but 90% of investors can’t hear them. While amateur traders obsess over daily spot fluctuations, professional uranium buyers are quietly locking in \$80/lb term contracts — a 23% premium to spot. This isn’t inefficiency. This is institutional money betting on mathematical certainty.

• Spot vs. Term Inversion: Current spot: \$64.83/lb. Current term: \$80/lb. When long-term contracts trade at massive premiums, that’s demand destruction at current prices. Utilities pay 23% more for future delivery because they understand what’s coming.

• Contracting Volume Collapse: Term contracting dropped to 45 million pounds in 2024, well below the 65–75 million pound replacement rate. This isn’t weakness — it’s procurement paralysis as buyers wait for policy clarity while supply windows slam shut.

• Technical Breakout: Uranium spot cleared \$81 resistance in late 2023 before policy uncertainty triggered consolidation. The 18-month base at \$50–65 is textbook institutional accumulation.

• Short Interest Explosion: Australian uranium miners — Paladin and Boss Energy — rank among ASX’s most shorted stocks. Record short interest during fundamental strength isn’t bearish sentiment. It’s rocket fuel for the next squeeze.

The psychology is textbook: fear dominates headlines while 5-year uranium performance shows +212% versus +25% for broad commodities. Retail sees recent weakness. Institutions see mathematical inevitability.

Key catalysts: The DOE allocated \$2.7 billion for domestic uranium purchases — the government acknowledging strategic vulnerability. AI data centre electricity demand is set to double by 2030 to 945 TWh, with nuclear projected to meet 35–62 GW of new demand by 2035. Japan has restarted 14 of 33 shuttered reactors, locking in 2.8 million pounds of new annual demand with 19 more in the pipeline. Kazakhstan announced a 17% production guidance cut for 2025.

When supply takes 15–20 years to develop but demand spikes in 3–5 years, that’s not a market — it’s a wealth transfer mechanism.

Your Uranium Wealth Decision: Mathematical Certainty vs. Emotional Paralysis

The uranium price forecast for 2025 isn’t speculation — it’s actuarial science. Every reactor under construction represents 200,000 pounds of locked annual demand. Every mine closure eliminates millions of pounds with geological certainty. The outcome is predetermined. Only the timing is negotiable.

\$10,000 invested at \$65/lb becomes \$21,500 at \$140 — the conservative analyst consensus target. Miss the move from \$65 to \$100, and you’ve missed 54% of the gains. Hesitation costs exponentially.

The Trump administration’s tariff uncertainty created the current buying opportunity. When policy clarity emerges — and it will — utility contracting resumes with vengeance. Maximum uncertainty equals maximum opportunity.

While retail investors panic over 13% year-to-date declines, term contracts at \$80/lb prove institutional conviction. Russian enrichment dominance guarantees eventual supply weaponisation. Chinese strategic reserve building removes millions of pounds from Western markets. US domestic production at 1% of consumption guarantees import dependency. This isn’t energy policy — it’s wealth redistribution from the unprepared to the positioned.

Your decision matrix is binary:

Option 1: Wait for “confirmation.” Watch prices climb from \$65 to \$80 to \$100 to \$140 while convincing yourself you’re “being cautious.” Join the majority who recognise bull markets only after missing the gains.

Option 2: Execute on mathematical probability. Position before contracting resumes. Accumulate during policy uncertainty. Become the beneficiary of crowd psychology rather than its victim.

The supply deficit isn’t a forecast — it’s physics. Reactor demand isn’t speculation — it’s construction schedules. Price appreciation isn’t hopeful — it’s inevitable.

The only unknown is whether you’ll be positioned when the mathematics resolves into profits.

The uranium market doesn’t care about your comfort zone. It only rewards preparation.