Currency War and Negative Rates: When Banking Logic Turned Upside Down

Updated Jan 23, 2026

When the Impossible Became Normal

Try this thought experiment: go back to 2008 and tell someone that within a few years, major central banks around the world would be charging people to hold their money. They’d probably look at you like you’d just escaped from a psychiatric ward. Yet here we are, living in a financial reality that would have seemed completely insane just a generation ago. Negative interest rates—once a theoretical curiosity discussed in dusty academic papers—have become standard operating procedure for central bankers worldwide.

The latest move in this global chess game? Back in 2016, China devalued the Yuan to five-year lows, adding more fuel to an already blazing currency war. This wasn’t some isolated decision—it was part of a coordinated global race to the bottom, with every major economy trying to weaken its currency to gain a competitive edge.

What did this mean for the Federal Reserve? Simple: they had no choice but to eventually join the party. Despite months of tough talk about “normalizing” policy and raising rates, the Fed’s messaging slowly shifted from “all is well” to “it’s not quite as good as we thought” and eventually to “oh my God, it’s actually pretty ugly out there and we need to do something drastic.” This script has been used repeatedly because it works beautifully on a population that’s been conditioned to accept whatever central bankers tell them.

Conditioning the Masses Like Pavlov’s Dogs

The general public has been trained remarkably well over the past decades, so there’s no reason to change the playbook now. Keep the narrative simple, repeat it constantly across all media channels, and people will swallow it completely. Mass psychology clearly demonstrates that crowds are fundamentally self-destructive—individuals with this mindset claim they want something better, but their actions consistently prove otherwise.

The central banking experiment has unfolded in distinct phases, each more extreme than the last. First came the prolonged low-rate environment that persisted for years. Then came the flood of money through quantitative easing programs that injected trillions into the financial system. The third phase got corporate America involved through massive share buyback programs, essentially enlisting companies to help pump up asset prices. Now we’re witnessing the fourth stage: negative rates designed to fuel what might become the mother of all bubbles.

Punishing Savers in the New Normal

Central bankers understand human psychology better than most people realize. They know that when uncertainty rises, people instinctively save more, even when doing so means accepting guaranteed losses. This fear-driven behavior persists even when banks start charging fees to hold deposits. People continue socking away money because uncertainty about the future overwhelms the pain of watching their savings slowly erode.

Many experts claimed that central bankers miscalculated—that negative rates were an unintended policy error. But the truth is far more calculated. This outcome was planned years in advance with meticulous precision. Watch how quickly the “we’re raising rates” narrative transformed into “actually, we need to cut rates again.” Even Fed Chair Yellen’s tone shifted noticeably more dovish with each passing month.

Plenty of economists have declared that negative rates are a terrible idea, and from one angle, they’re absolutely right. If you sit passively and take no action, you’re guaranteed to lose. But here’s where it gets interesting: if you’re proactive and understand the game being played, negative rates can actually work in your favor. Consider this Danish family that’s literally getting paid interest on their mortgage instead of paying the bank. They’re being compensated to borrow money to buy a house. Let that sink in for a moment.

How Cheap Money Inflates Everything

Artificially cheap money inevitably leads to speculation, and the stock market provides the perfect venue for that speculation. Expect corporations to borrow even more aggressively at these absurdly low rates and use those funds to repurchase their own shares, artificially inflating earnings per share in the process. There’s virtually no accountability left on Wall Street, and since executive compensation is directly tied to stock performance, you can bet these incentives will be fully exploited.

Corporate officers will do whatever it takes to boost share prices, even if it means creating an elaborate illusion that earnings are rising when they’re actually flat or declining. They want to cash in their options and bonuses—the small investor is simply collateral damage in this game. It’s straightforward, and Congress has essentially blessed this behavior as legal, so nothing’s stopping it and everything encourages it. We’ve covered this dynamic extensively over recent years, consistently arguing that every market pullback should be viewed as a buying opportunity rather than a reason to panic.

The Property Price Explosion Nobody Saw Coming

Negative rates dramatically lower mortgage costs, and in some cases, borrowers actually receive checks from banks as interest payments on their home loans. This isn’t theoretical—negative rates are already fueling a genuine property bubble in Sweden, a phenomenon we’ve documented previously. Property prices have also been surging in the U.K., so it’s only a matter of time before we see the same dynamics playing out across the U.S. market.

Banks will almost certainly lower lending standards in the United States as competition for borrowers intensifies. We’ve already seen this beginning—Barclays Bank announced 0% down payment mortgages, essentially removing the traditional barrier to homeownership. If that sounds familiar, it should. We’ve been down this road before, and it didn’t end well last time.

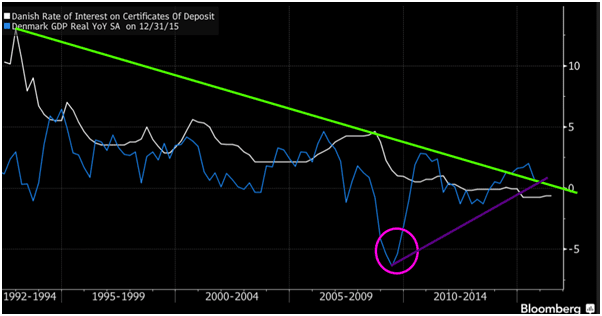

The GDP Illusion That Actually Works

The claim that negative rates can improve GDP sounds completely insane on its face. Yet the data tells a different story. The chart below shows Denmark’s experience clearly—negative rates do create the compelling illusion that the economy is functioning well, and remarkably, the population seems to accept this reality without much protest.

Denmark’s GDP began rising shortly after implementing negative rates, which was precisely the intended outcome. Notice how immediately following the 2008-2009 crisis, rates were slashed faster than at any previous period in the last two decades. The lower rates dropped, the higher GDP climbed—in fact, you can clearly see it established an upward trend that persisted for years.

Reading the Global Game Board

China’s decision to devalue the Yuan demonstrates clearly that the “devalue or die” strategy has been embraced by every major economy worldwide. Nations will continue weakening their currencies to maintain competitive positions because the global economy remains fundamentally weak. Only hot money—speculative capital chasing returns anywhere they can be found—creates the illusion that all is well.

Mass psychology reveals that crowds would rather hear a comforting lie than face an uncomfortable truth. In that sense, they’re getting exactly what they secretly desire: markets that look magnificent from the outside while being completely rotten at the core. Since the United States hasn’t fully embraced negative rates yet, this market still has substantial upside potential remaining.

The Fundamental Disconnect Nobody Wants to Acknowledge

This market won’t soar higher because of strong fundamentals—from a fundamental perspective, it should be in the toilet. It will climb because of hot money flooding the system and chasing any assets that offer positive returns. We expect property prices to continue their upward march in the U.S., and once lending standards are inevitably lowered further, another full-blown property bubble will likely develop.

Regarding equities, sentiment remains surprisingly negative despite elevated prices, and significantly more capital will flow into stocks once negative rates become widespread domestically. Therefore, the prudent contrarian investor who doesn’t let emotions override logic should view all significant pullbacks and corrections as prime buying opportunities rather than reasons to flee.

Which means that this market will fly to the moon one day before it crashes to Hell. The average person is too busy sucking his thumb and watching TV (Khardishans and other crap) to realize what’s going on.

Thoroughly enjoy your take. Thanks for posting.

You are welcome. Slowly more individuals are coming on board to the idea that this market is being driven higher by pure fraud; in other words, hot money that is created out of thin air

You seem to have a good grasp of what’s going on

Excellent explanation of rates and futures. I wish I could find a good explanation of where the USD vs CAD valuation will be in the future, so I can decide when to exchange my CAD to USD.