The 18-Year Rhythm: Decoding Housing Market Cycles

Oct 31, 2024

In 1818, a parcel of Manhattan farmland sold for $2,000. By 1836, that same plot commanded $80,000—then crashed to $25,000 by 1840. This pattern repeated in 1854, 1872, 1890, 1907, and beyond, each cycle lasting approximately 18 years. What mysterious force drives these predictable housing market fluctuations, and why do they persist with such remarkable regularity?

Economist Homer Hoyt first documented this phenomenon in 1933, noting that Chicago real estate prices followed a precise 18-year cycle dating back to 1830. Fred Harrison later expanded this research, demonstrating the pattern’s persistence across multiple countries and centuries. The cycle typically consists of 14 years of price growth followed by 4 years of recession or stagnation.

Recent data reinforces this pattern: 1972 crash, 1990 downturn, 2008 collapse, and projected 2026 adjustment. Each cycle shares remarkable similarities in its progression through distinct phases.

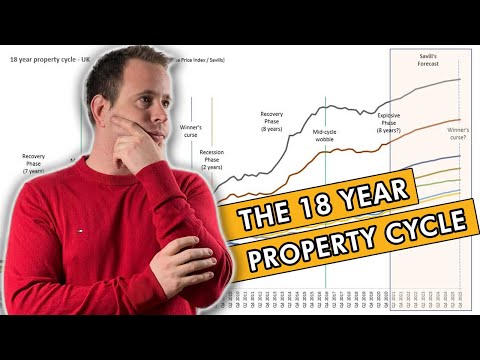

The Four Phases of Housing Cycles

Real estate data from 1800 to 2023 reveals distinct patterns in housing market behaviour. The first phase, Recovery, typically lasts 7 years. During the 1933-1940 recovery period, U.S. housing prices rose 49% after falling 30% during the Great Depression. Similarly, from 2012 to 2019, following the 2008 crash, median home prices increased from $154,700 to $274,600, representing a 77.5% recovery.

The second phase, the Mid-Cycle Dip, usually spans 12-18 months. Despite strong economic indicators in 1994, housing prices decreased by 2.8% nationally. This pattern repeated in 2014 when prices dipped 3.1% amid positive GDP growth. The Federal Reserve’s data shows these mid-cycle corrections occurred without triggering broader economic recessions.

The Expansion phase, lasting approximately six years, shows remarkable consistency. 1996-2002, before the notorious bubble, housing prices rose 45.3% nationwide. The 2015-2021 expansion saw median home prices surge from $298,900 to $408,800, marking a 36.8% increase. During these periods, mortgage rates averaged 6.1% and 3.8%, respectively, according to Freddie Mac’s historical data.

The Hypersupply and Recession phase presents clear statistical patterns, typically lasting 4 years. The 1989-1993 downturn saw prices fall 14.3% nationally. The 2007-2011 crash witnessed a more severe 33.8% decline. Census Bureau data shows building permits dropped 73% during this phase in 2008, compared to 58% in 1991.

Regional variations add complexity to these phases. During the 2008 crash, while Nevada experienced a 60% price decline, Texas saw only a 12% reduction. The Federal Housing Finance Agency’s state-by-state index reveals similar disparities in recovery rates: California’s home values recovered in 6 years post-2008, while Michigan took 11 years to reach pre-crash levels.

Construction data correlates strongly with cycle phases. Building permits typically increase by 156% during recovery, peak during expansion with an average of 1.8 million annual starts, and then plummeted by 65% during the recession. The National Association of Home Builders reports that builder confidence follows a similar pattern, averaging 72 during Expansion phases and dropping to 12 during Recessions.

Mortgage default rates provide another reliable indicator. During Expansion phases, default rates average 1.2%. This figure tripled during the early Recession phases, reaching peaks of 8.1% in 1932 and 10.1% in 2010. The S&P/Case-Shiller Home Price Index shows that prices typically fall six months after default rates exceed 4%.

Land value fluctuations amplify these phases. Urban land prices historically rise 4.3 times faster than building costs during Expansion phases and fall 3.2 times more rapidly during Recessions. Federal Reserve data shows land values represented 47% of total property value in 2006, dropping to 31% by 2011 before climbing back to 41% in 2019.

Mass Psychology’s Role

The cycle’s regularity stems partly from human nature. As prices rise, memories of previous crashes fade. The 2005-2007 period demonstrated this perfectly—despite clear warning signs, buyers rushed into the market, convinced “this time is different.” Bank lending standards loosened, with subprime mortgages reaching $600 billion in 2006, up from $160 billion in 2001.

Specific metrics consistently signal cycle peaks. When housing prices outpace wage growth by 2:1, corrections typically follow. In 2007, the price-to-rent ratio hit 1.8 times its historical average. Similar ratios appeared before the 1990 and 1972 downturns.

Building permit data provides another reliable indicator. Peaks in permit applications occurred 18-24 months before major price corrections in 1989, 2006, and 2020.

The Credit Cycle Connection

Federal Reserve data shows that mortgage lending volumes follow predictable patterns within the 18-year housing cycle. During the 2002-2007 boom, mortgage originations increased from $2.2 trillion to $3.8 trillion annually. By 2008, this figure plummeted to $1.4 trillion, marking a 63% decline. Similar patterns emerged in previous cycles, with lending volumes dropping 47% between 1989 and 1990.

Interest rate fluctuations dramatically influence buying power. When rates dropped from 6.5% to 3.3% between 2008 and 2012, the average homebuyer’s purchasing power increased by $114,000 on a $300,000 mortgage. According to Freddie Mac’s records, each 1% decrease in mortgage rates historically translates to an 11% increase in qualified buyers entering the market.

Credit standards exhibit cyclical behaviour. The Mortgage Bankers Association’s data reveals that the average FICO score requirement for approved mortgages dropped from 720 in 2000 to 680 in 2006. During the 2008 crisis, this threshold surged to 760. Down payment requirements followed similar patterns, falling from 20% to as low as 3% during boom periods, then rising sharply during busts.

Bank lending practices show clear correlations with housing cycles. In 2006, subprime mortgages represented 23.5% of all originations, compared to 7.9% in 2002. The Office of the Comptroller of the Currency reports that loan-to-value ratios exceeded 95% for 29% of mortgages in 2007, dropping to 7% by 2009. These metrics have proven reliable indicators of impending market shifts.

Credit default swap (CDS) prices offer early warning signals. The ABX index, tracking subprime mortgage securities, began declining in late 2006, months before housing prices peaked. CDS spreads on mortgage-backed securities widened from 20 basis points in 2006 to over 300 basis points by mid-2007, signalling growing credit risk concerns.

Commercial real estate lending follows similar patterns. Federal Reserve Bank data shows commercial real estate loan volumes increased 60% between 2004 and 2008, then contracted 37% over the following two years. Small bank exposure to commercial real estate loans peaked at 357% of risk-based capital in 2007, falling to 281% by 2010.

Consumer credit behaviour mirrors housing cycles. TransUnion data indicates that mortgage delinquency rates typically begin rising two years before price peaks. In 2006, while housing prices were still climbing, early-stage delinquencies increased 12%, foreshadowing the coming crisis. Credit card utilization rates show similar predictive value, peaking at 27% above historical averages before major housing downturns.

International credit flows amplify these cycles. Bank for International Settlements data reveals that cross-border real estate investment increased 278% between 2000 and 2007, with foreign buyers accounting for 18% of U.S. residential property purchases by value in 2007. During the subsequent crash, this figure dropped to 4.3% by 2009.

Geographic Variations and Local Markets

While the 18-year cycle manifests nationally, local markets show distinct variations. Coastal cities typically lead price movements by 12-18 months. San Francisco home prices peaked in 2006, preceding the national peak by 16 months. Understanding these regional differences offers strategic advantages for investors.

Each phase demands different approaches. Early recovery periods favour bulk purchases and renovation strategies. Mid-cycle benefits development projects. Late-cycle requires careful asset selection and increased cash reserves. Real-world success stories abound—investors who bought in 2009-2011 saw average returns exceeding 140% by 2017.

Policy interventions affect but don’t prevent the cycle. The 2020 pandemic prompted massive stimulus, including $2.3 trillion in Fed mortgage purchases. While this delayed the cycle’s natural progression, historical patterns suggest it postponed rather than prevented the next adjustment.

Looking Forward: The 2026 Projection

Current housing market data points to significant patterns emerging toward 2026. The Federal Reserve Bank of St. Louis reports that the home price-to-rent ratio reached 1.71 in 2023, exceeding the 1.68 level recorded in 2006. U.S. Census Bureau data shows new home sales hitting 616,000 units annually in 2023, compared to the peak of 1.28 million in 2005.

Mortgage rate trends reveal striking parallels. In 1989, rates averaged 10.32%, dropping to 7.81% by 1994. Similarly, rates rose from 3.11% in 2021 to 7.79% in October 2023. Freddie Mac’s historical data indicates that such rapid rate increases typically precede significant market adjustments within 30-36 months.

Demographics mirror previous cycle peaks. According to the National Association of Realtors, the millennial generation, aged 27-42 in 2023, represents 43% of home buyers. This mirrors the Baby Boomer concentration of 44% during the 1989 cycle peak. Population data shows 72.1 million Millennials entering peak earning years, comparable to 71.6 million Boomers in the late 1980s.

According to the Producer Price Index, construction costs have risen 35.6% since 2020. Similar spikes occurred between 1986-1989 (31.2%) and 2004-2007 (29.8%). The National Association of Home Builders reports that material costs alone added $18,600 to the price of an average new home in 2023.

Inventory levels show concerning trends. The months’ supply of homes stood at 3.3 months in late 2023, below the balanced market threshold of 6 months. During previous cycle peaks, inventory reached 4.5 months (1989) and 7.2 months (2006) before price corrections began. Realtor.com data indicates active listings are 41% below pre-pandemic levels.

Affordability metrics signal stress. The median home price reached 7.2 times median household income in 2023, surpassing the 2006 ratio of 6.8. The Atlanta Federal Reserve’s Home Ownership Affordability Monitor shows that the typical American household now needs to spend 43.2% of income on mortgage payments, exceeding the previous record of 41.2% in 2006.

Investment patterns echo previous cycles. According to ATTOM Data Solutions, the share of all-cash purchases hit 32% in Q3 2023, approaching the 34% level seen in 2005. Corporate buyers acquired 28% of single-family homes sold in 2023, compared to 17% in 2019, mirroring the surge in institutional buying before previous corrections.

Regional market data reveals familiar patterns. Coastal markets show price-to-rent ratios exceeding 2005-2006 levels by 15-20%. The Case-Shiller index indicates that cities like Phoenix, Las Vegas, and Miami – historically volatile markets – have seen price appreciation 45% above the national average since 2020, similar to patterns observed before previous corrections.

Practical Applications

Understanding this cycle offers strategic advantages:

– Buy during years 1-5 of the recovery

– Develop during years 6-10

– Sell or refinance during years 11-14

– Maintain liquidity during years 15-18

Conclusion

The 18-year housing cycle’s persistence across centuries offers both warning and opportunity. While each cycle has unique characteristics, the underlying pattern remains remarkably consistent. Success in real estate investment requires understanding these rhythms and positioning accordingly. As we approach the next projected turning point, this knowledge becomes increasingly valuable for investors, homeowners, and market participants.