Oops Loan Predicament: The Recurring Subprime Auto Loan Crisis

Updated Dec 17, 2023

We will delve into this topic against a historical backdrop, guided by the age-old saying that “those who fail to learn from history are doomed to repeat it.” We find ourselves in a situation reminiscent of the past, as many individuals opted for variable loans at low interest rates, only to face significant challenges as rates surged.

Intro

“Greed and Recklessness Still Rule the Markets: No Lessons from 2008, and History May Repeat Faster Than Expected—Fitch Warns of 20-Year High in Subprime Auto Bond Delinquencies.

In the world of finance, some lessons are never learned. Despite the disastrous 2008 crash, fueled by unchecked greed and recklessness, history’s warnings seem to have fallen on deaf ears. The stage is set for déjà vu, and this time, it might be even swifter and more devastating.

Picture this: The stock market’s frenzied rise, reminiscent of the days preceding the 2008 crisis, as investors chase after quick gains with little regard for underlying risks. It’s a high-stakes game of chicken that could push the economy to the brink again.

Fitch Ratings recently dropped a bombshell: Subprime auto bond delinquencies are now at a shocking 20-year high. This isn’t just a red flag; it’s a blaring siren, warning of impending financial turbulence. Despite this warning, the intoxicating allure of profit continues to overshadow prudence.

The financial world is again on the precipice, and the question remains: Have we truly learned from the past, or are we condemned to repeat our mistakes? The answers lie in the choices made by those who hold the reins of the market’s fate.

Oops Loan Alert: Subprime Auto Crisis Looms, Echoes of 2008 in the Financial Landscape

The issue of subprime auto loans and the potential for a recurring crisis is a matter of concern in the financial landscape. Some argue that the lessons from the 2008 financial crisis have not been fully absorbed, leading to greed and recklessness continuing to influence market behaviour.

Some observers believe history is bound to repeat itself, and a subprime auto loan crisis could unfold sooner than expected. Fitch, a prominent credit rating agency, has reported that delinquencies in subprime auto loan bonds have reached a 20-year high. This indicates a significant level of non-payment or late payment by borrowers in this segment.

The rise in subprime auto loan delinquencies raises concerns about the quality of loans being issued and the ability of borrowers to meet their repayment obligations. It also highlights potential risks for financial institutions and investors who may hold these loans or securities backed by them. If the trend continues and defaults escalate, it could have broader implications for the financial system’s stability.

However, it is essential to note that differing viewpoints exist regarding the severity and potential impact of the subprime auto loan situation. Some argue that the current situation does not necessarily indicate a crisis on the same scale as the subprime mortgage crisis of 2008. They emphasize that subprime auto loans represent a smaller portion of the overall debt market and have distinct characteristics compared to subprime mortgages.

Nonetheless, the rising delinquency rates in subprime auto loans warrant attention and ongoing monitoring. Regulators, financial institutions, and investors should remain vigilant to assess potential systemic risks and take appropriate measures to ensure the stability and resilience of the economic system.

Ultimately, the extent and consequences of the subprime auto loan predicament will unfold over time. Continued analysis and scrutiny of market dynamics, lending practices, and borrower behaviour will be essential in understanding the evolving situation and mitigating potential risks.

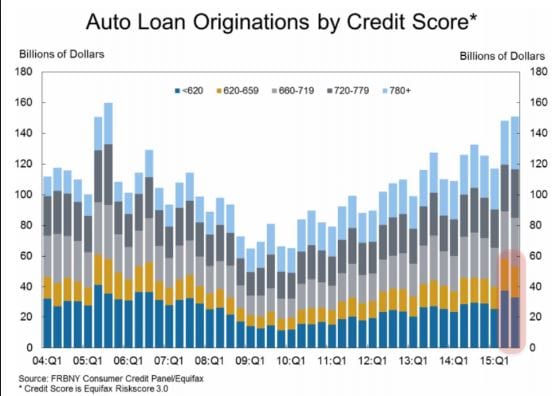

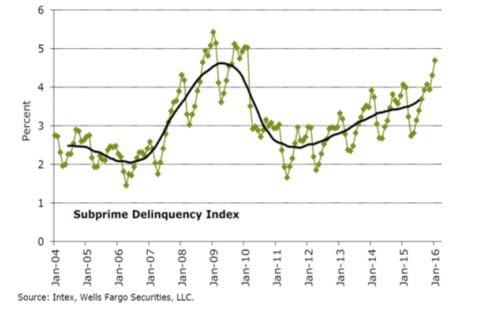

Behold This Chart: Unveiling the ‘Great’ Things (Prepare for Sarcasm)

A Startling Surge: Auto Payment Delinquencies Soar by 11.6% Year Over Year, Reaching a 5.16% Delinquency Rate.

In a striking twist of fate, the current delinquency rate surpasses the 5.04% peak seen during the tumultuous days of the 2008 financial crisis, as reported by Fitch. It’s a stark validation of a long-held argument: Our so-called ‘recovery’ is nothing more than a shimmering illusion.

This illusion is meticulously crafted, fueled by what can only be described as ‘hot money.’ With interest rates kept artificially low, the logical choice for any rational individual or business is to embrace speculation, seeking higher yields in a world awash with easy cash.

The numbers don’t lie; the financial landscape dances on a precipice. It’s a story of surging delinquencies and an economic reality that’s more smoke and mirrors than substance. The question that looms is whether we’ll learn from the past or find ourselves trapped in yet another web of illusions.

This chart further illustrates the deteriorating picture.

Our concern doesn’t solely revolve around the performance of individual transactions; instead, it’s about how a collective of mid-sized and smaller issuers might simultaneously face funding risks, leading to unforeseen consequences for investors,” emphasized Duignan. “This scenario could trigger a vicious cycle where investors pull away from smaller companies, putting pressure on them to reduce their servicing costs, ultimately resulting in increased loan losses.”

Investors generally enter this territory with an awareness of the inherent risks, attracted by the promise of higher yields. However, the outlook can swiftly change when losses become a reality. Anticipating a loss is one thing, but dealing with one is entirely different. If delinquencies begin to surge, investors might abruptly exit the market, leaving it empty of buyers. As the saying goes, it’s always the calmest before the storm.

If you have investments in this sector, it may be prudent to consider hedging your positions by acquiring some puts, essentially shorting the auto loan sector.

Central Bankers’ Hidden Agenda – Or Perhaps Not So Hidden After All

The Federal Reserve’s consistent theme has been a downward trajectory in interest rates. The occasional talk of raising rates seemed like a facade, an attempt to paint a rosy picture of economic health. This strategy was devised to give the U.S. dollar the appearance of strength compared to other currencies, positioning us as the last bastion against negative rates.

The underlying plan was to manoeuvre central bankers worldwide into a corner, compelling them to consider negative interest rates. Having seemingly achieved this goal, the Fed is now retracting its hawkish stance and returning to a dovish one. The next logical step in this complex game plan is to lower rates further, ultimately aiming for negative territory.

It’s a strategy that has kept economists and financial analysts on their toes, revealing a deeper chess game behind the scenes of monetary policy. As we watch the Fed’s moves, the question remains: How far will central bankers go to navigate the global economy’s future?

Central bankers have exhibited a masterful strategy in this high-stakes game of monetary chess. By skillfully manipulating interest rates, they’ve navigated economic uncertainties and wielded a significant impact on the world stage. The apparent U-turn in policy from hawkish to dovish signals a deeper intention. With negative rates on the horizon, the Federal Reserve’s plan may hold more surprises, fundamentally reshaping the financial landscape.”

Implications of Lower Rates

Lower interest rates trigger a ‘hot money’ surge into the markets. Companies enticed by cheaper borrowing costs embark on massive share buyback programs, creating the illusion of prosperity. This buyback strategy artificially inflates earnings per share (EPS) without genuine improvements in efficiency or increased product sales. However, these actions push individuals on fixed incomes into risky speculation, a group that can least afford it.

Ironically, this cohort, drawn into the markets by desperation, is often the most vulnerable to significant financial losses. When they eventually enter the speculative fray, markets are prone to crest, potentially erasing most, if not all, of their savings. This cruel twist creates a new class of individuals financially bound to a system they might otherwise resist.

Resistance gives way to dependency on the state, as these individuals have no choice but to accept the flawed system. This dependence weakens opposition, further entrenching the status quo.”

The Impact of Higher Interest Rates on Auto Loans and Delinquencies

The interest rate level significantly influences various aspects of the economy, including auto loans and delinquency rates. While lower rates can stimulate borrowing and market activity, higher rates can have contrasting effects. This article examines the implications of higher interest rates on auto loans and delinquencies and the potential challenges faced by individuals and the financial system as a whole.

Higher interest rates lead to increased borrowing costs for consumers seeking auto loans. As rates rise, financing a vehicle purchase becomes more expensive. This can impact the affordability of monthly payments and potentially deter some consumers from taking out auto loans.

With higher borrowing costs, the demand for new and used cars may decline. Higher interest rates can discourage potential buyers from making large purchases, leading to a slowdown in the automotive industry. This can have implications for automakers, dealerships, and related industries.

Rising interest rates can pressure borrowers, particularly those with adjustable-rate auto loans or subprime credit. As monthly payments increase, some individuals may struggle to meet their financial obligations, resulting in higher delinquency rates. Delinquent auto loans can negatively impact lenders, leading to potential losses and increased financial risks.

Economic Impact and Consumer Spending:

Higher interest rates can have broader economic consequences, impacting not only individual borrowers but also various sectors of the economy. As consumers allocate more of their income towards debt repayment due to increased borrowing costs, discretionary spending tends to decrease, leading to a potential cascading effect on multiple industries.

One sector that can be significantly affected is retail. When consumers have less disposable income for non-essential purchases, retail businesses may experience a decline in sales. Retailers offering luxury goods or non-essential items are particularly vulnerable, as consumers prioritize essential expenses and debt obligations over discretionary spending. This reduction in consumer demand can lead to inventory accumulation, profit margin compression, and potential job losses within the retail sector.

The hospitality industry, including restaurants, hotels, and tourism, can also feel the impact of decreased consumer spending. As individuals tighten their budgets, they may dine out less frequently, opt for more affordable accommodation options, or reduce leisure travel. This can result in reduced revenue for hospitality businesses, leading to potential downsizing, reduced investment, and a slowdown in economic activity within the sector.

Furthermore, the entertainment industry, which encompasses activities such as concerts, movies, and recreational events, can experience a decline in attendance and revenue. Higher interest rates may make consumers more cautious about discretionary entertainment expenses, leading to lower ticket sales and reduced demand for entertainment services. This, in turn, can ripple effect on jobs and investments within the industry.

The cumulative impact of reduced consumer spending across these sectors can contribute to an economic slowdown. When businesses experience decreased revenue and profitability, they may respond by scaling back operations, postponing expansion plans, or even implementing workforce reductions. Job losses within affected industries can lead to declining consumer confidence, further dampening spending and economic growth.

It is important to note that the magnitude of the impact may vary depending on the overall economic conditions, consumer sentiment, and the specific industry dynamics. Additionally, other factors such as government policies and global economic trends can also influence the overall financial impact of higher interest rates on consumer spending.

Shift the Focus to Investment: Say Goodbye to Oops Loans

In today’s world, the illusion of an economic recovery is perpetuated through substantial liquidity infusions. Within this financial landscape, one cannot ignore the inevitable outcome. It becomes increasingly apparent that another financial crisis is on the horizon. Therefore, it is highly advisable to consider the acquisition of gold bullion as a prudent financial strategy.

Gold, often referred to as the “safe haven” asset, has historically demonstrated its resilience during economic turmoil. It serves as a reliable hedge against the uncertainties that accompany financial crises. By holding gold bullion, individuals can safeguard their wealth and financial security in the face of economic downturns and market volatility.

Investing in gold bullion is a strategic move to protect one’s assets and financial well-being. As we navigate the unpredictable currents of the global economy, this precious metal stands as a dependable anchor, providing a sense of security and stability in an otherwise uncertain financial landscape.

Originally published on August 26, 2020, this article has been periodically updated. The latest update was conducted on Dec 17, 2023, ensuring the information remains current and relevant.

Unconventional Articles Worth Exploring

Rational Thinking Definition: Unleashing the Power of Reason

What Time is the Best Time to Invest in Stocks? When Fools Panic

How Does Your Account Growth Demonstrate The Importance Of Investing Early?

What Do People Buy During a Stock Market Panic?

Greater Fool Theory of Investing: The Endless Cycle of Folly

How to Read Candlesticks: Unlock Hidden Market Moves

Uncovering the Truth: Market Experts Clueless

Pavlov’s Theory in Action: Herds Act Like Fools, Not Wisemen

Where Does the Money Go When the Stock Market Crashes: A Contrarian Perspective

What Kinds of Behaviors Can Prevent People from Making Smart Investing Decisions?

How to Overcome Fear of Investing: Think Independently, Succeed Confidently

Wolf vs Sheep Mentality: Embrace the Hunt or Be the Prey

The Dummies Guide to Investing: A Practical Guide for Beginners

How much money do i need to invest to make $4,000 a month?

Define Contrarian Thinking: Challenging the Norms for Success

Breaking Free: How Avoiding Debt Can Lead to Financial Freedom & Hope

Flash Crash: Exploit the Chaos and Outperform the Crowd

Mass Psychology & Financial Success: An Overlooked Connection