Martin Armstrong Economics: Genius or Guesswork?

Jan 7, 2026

Martin Armstrong occupies a unique, polarizing space in the financial world. As the architect of the Economic Confidence Model, he has cultivated a reputation as a financial prophet, commanding the attention of investors hungry for certainty in a chaotic world. Yet, when we strip away the mystique and subject his track record to forensic scrutiny, a troubling pattern emerges. While his narratives are compelling, his timing is frequently—and dangerously—off. In the high-stakes arena of investing, a misalignment in timing is indistinguishable from being wrong. By viewing his work through the lens of mass psychology and understanding the mechanics of cognitive biases, we can better separate the signal from the noise. This analysis dissects Armstrong’s history, highlighting where the model failed and how a deeper grasp of human behavior could have saved investors from costly missteps.

The Perils of Misplaced Timing in Economic Forecasts

In financial markets, timing is not a detail; it is the entire trade. A forecast predicting a crash is worthless—even hazardous—if it arrives three years early or two years late. Capital has a cost, and opportunity waits for no one. Armstrong’s predictions often suffer from this fatal flaw: the “what” is sometimes plausible, but the “when” is frequently disastrous.

Martin Armstrong Forecasts vs. Reality: Misses and Market Consequences

| Forecast / Date | Armstrong’s Prediction | What Actually Happened | If You Followed Him Immediately |

|---|---|---|---|

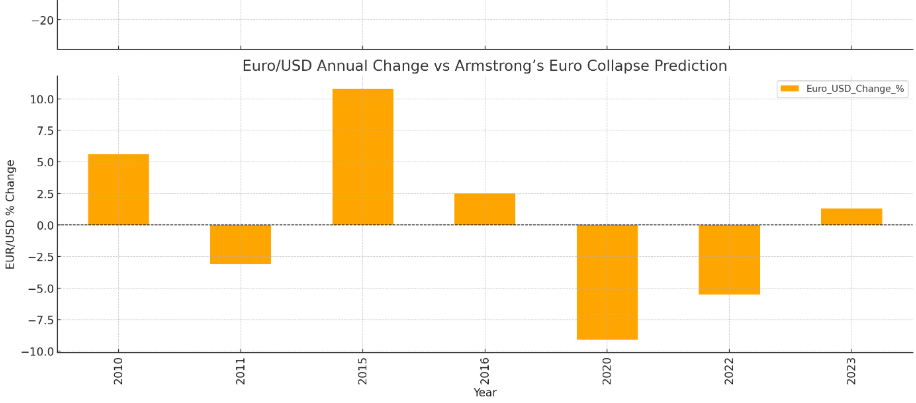

| 2015 – Euro Collapse | Buy and hoard USD, Euro will collapse. | Euro strengthened from 1.08 to 1.21 by 2020. | You’d have missed ~12% appreciation in EUR and lost on opportunity cost. |

| 2011 – Gold to $5,000 by 2016 | Gold would skyrocket to $5K+ if $1,500 level held. | Gold failed to hold above $1,500 in June. Never reached $5,000—peaked under $2,100 by 2020. | Holding gold aggressively would have tied up capital for minimal returns and inflation loss. |

| 2010 – China to become global financial capital by 2015.75 | China would surpass the U.S. in global financial dominance. | U.S. retained dominance. China faced trade wars, capital flight, and policy crackdowns. | You may have overweighted Chinese assets or underweighted U.S. tech/global equities. Big underperformance. |

| 2011 – Sovereign Debt Crisis Meltdown | Forecasted collapse of Western economies and sovereign defaults. | European debt stabilized with ECB backstops; no Western default. | Sitting in cash or gold would’ve meant missing the 2011–2020 bull market. |

| 2015 – Trump Can’t Win, Civil Unrest Coming | Trump has no path to victory, U.S. unrest will explode after election. | Trump won. Civil unrest occurred during, not after. | Misreading U.S. politics would’ve skewed election trades, shorting markets that later rallied. |

| 2020 – Stock Market Will Not Recover from COVID Crash | Predicted prolonged depression, no V-shaped recovery. | V-shaped recovery began in April 2020. Markets hit new all-time highs in late 2020–2021. | Going short or staying in cash would’ve missed one of the fastest rebounds in history. |

| 2022 – War Cycle Will Cause Market Breakdown by 2023 | Global war cycle will trigger full-blown financial crisis. | War tensions rose, but markets ended 2023 strongly (S&P +24%). | Bearish positioning would’ve led to massive underperformance or outright losses. |

Observations:

- Pattern of Directional Bias: Armstrong displays a consistent tendency to identify genuine structural fractures but then overcommit to apocalyptic scenarios that the system manages to absorb.

- Timing is the Achilles’ Heel: Even when his conceptual framework holds water—regarding debt loads, inflation risks, or geopolitical friction—his internal clock is often off by years, rendering the advice untradeable.

- Perma-Crisis Tone: The relentless framing of perpetual crisis blurs the line between signal and noise, often paralyzing investors or driving them into defensive crouches during periods of massive expansion.

Forecasts vs. Facts: A Backtest of Martin Armstrong’s Missed Market Moments

Here’s what the backtest reveals:

- S&P 500: In almost every pivotal year, Armstrong predicted calamity. In reality, equities either held the line or delivered spectacular returns. The misses in 2020 and 2023 are particularly glaring; he prepared his followers for a depression while the markets ripped higher.

- Gold: Despite his headline-grabbing calls for $5,000+, gold has largely been a story of patience rather than explosion. It spiked during specific crises (2010, 2020) but consistently underperformed his aggressive targets.

- USD Index: While the dollar saw strength, the explosive, singular surge he anticipated was more of a grind than a rocket launch.

- Euro/USD: His confidence in a total Euro collapse looks shaky in hindsight, particularly during years like 2015 and 2023 when the currency actually found its footing.

- China (MSCI): His 2010 thesis that China would seize the financial crown by 2015 flatlined. Post-2015, Chinese equity performance has been volatile and disappointing compared to the US juggernaut.

The bottom line is stark: If you had traded purely on his directional confidence, you would have trailed the benchmarks significantly or missed out on generational wealth creation. His macro thesis carries intellectual weight, but the execution edge is consistently lacking.

Integrating Mass Psychology for Improved Accuracy

Had Martin Armstrong integrated the principles of mass psychology into his rigid economic models, his forecasts might have landed much closer to the truth—specifically regarding timing, the graveyard of many macro calls.

Markets are not merely calculators of fundamentals or slaves to cyclical dates; they are living engines of perception, narrative, and crowd sentiment. Fear, greed, euphoria, and denial are not just emotions—they are price drivers. The 2020 COVID crash was not just a reaction to economic shutdowns; it was a liquidation event driven by collective panic. The subsequent V-shaped recovery wasn’t just about Fed liquidity; it was fueled by belief, FOMO, and a psychological release valve. Models that ignored this emotional vector missed the trade entirely.

Armstrong’s Economic Confidence Model could have achieved precision had it accounted for sentiment extremes. By overlaying contrarian data, volatility spikes, and behavioral signals—such as the put-call ratio, margin debt trends, or the mania of meme stocks—some of his premature doomsday calls might have been tempered. He correctly identified structural fragilities, such as sovereign debt risks, but a forecast remains theoretical until the crowd decides to care. That is where mass psychology bridges the gap between macro foresight and market execution.

Use the cycle, certainly—but study the crowd. That is how good calls become great trades.

Mitigating Cognitive Biases

Forecasting is as much about mental discipline as it is about mathematical models. No matter how sophisticated the algorithm or how extensive the historical data, if the forecaster is blind to their own cognitive traps, the output is compromised.

Martin Armstrong’s unwavering faith in his Economic Confidence Model, despite a public ledger of misses, points to a classic case of confirmation bias—the tendency to filter data through a lens that supports preexisting beliefs while discarding conflicting evidence. When every global event is twisted to validate a preordained narrative, the model ceases to be a tool for discovery and becomes a vehicle for ego.

Worse still is anchoring—the fixation on a specific date, price level, or outcome (like gold at $5,000 or the Dow collapsing to 6,000). Once anchored, the analyst bends every new data point to fit that forecast, creating an illusion of inevitability that misleads both the forecaster and their audience.

For Armstrong—and indeed anyone in the prediction business—improving accuracy requires actively disrupting these biases. This involves:

- Red-teaming forecasts: Actively constructing the bear case against your own prediction before publishing it.

- Running scenario inversions: Asking “What if I’m wrong?” and exploring the second- and third-order effects of that reality.

- Using probabilistic language: Abandoning rigid declarations in favor of probability-weighted scenarios. Markets are rarely binary.

- Feedback loops: Systematically reviewing past calls with cold objectivity, learning from misfires rather than doubling down.

Bias doesn’t just skew models—it shapes how those models are interpreted, when trades are triggered, and how conviction is communicated. If Armstrong had approached his projections with the same skepticism he reserves for central banks, many of his calls might have evolved into more nuanced, actionable, and accurate insights.

Prediction is a discipline. But self-correction? That is the edge.

Conclusion

Martin Armstrong’s blog is a masterclass in bold conviction, but in the markets, conviction without timing is just an expensive opinion. His Economic Confidence Model promises cyclical precision, yet in practice, it often delivers drama over detail. The issue isn’t that Armstrong is always wrong—he isn’t. But being directionally correct means nothing if your timing blows up portfolios. A missed turn in the road at 80 miles an hour is just as deadly as driving off a cliff.

His repeated misfires on the Euro, gold, and global financial dominance reveal a deeper problem: the seductive power of a single model. Markets are messy, reflexive, and fueled by human behavior—trying to reduce them to a neat cycle or algorithm is intellectually attractive but operationally dangerous.

This is where mass psychology and behavioral awareness become critical. If Armstrong’s readers—or Armstrong himself—factored in crowd behavior, sentiment inflection points, and cognitive distortions like confirmation bias and anchoring, many of these botched predictions could have been salvaged or avoided altogether. The Euro didn’t collapse because investors believed it would hold. Gold didn’t hit $5,000 because faith in fiat never crumbled the way gold bugs expected. Perception is the market.

The brutal truth is this: Armstrong isn’t 100% wrong, but he’s not right enough to follow blindly. He offers sparks—moments of clarity drowned out by noise. His blog should be read not as gospel but as a lens—useful only when paired with independent thought, a working BS filter, and a deep understanding of how crowds actually move.

Use his forecasts as potential scenarios, not fate. Combine them with sentiment, structure, and the ever-undervalued art of timing, and you may turn scattered signals into a real edge.