A Day Late and A Dollar Short

Updated Oct 2023

Introduction

The analogy of “a day late and a dollar short” aptly reflects how the U.S. government and central bankers have eroded the dollar’s purchasing power since its inception. Much like arriving after the ideal moment has passed, the dollar’s value now falls significantly short compared to its historical position when backed by gold. This decline signifies a temporal delay and a considerable reduction in real value, with the dollar purchasing nearly 90% less than it did during the gold-backed era.

In financial terms, the government’s actions can be likened to being tardy and insufficient, resulting in missed opportunities and an inability to meet the required standard. The phrase underscores the consequences of delayed or inadequate responses, emphasizing the importance of proactive and timely measures. The erosion of the dollar’s purchasing power is a cautionary tale, illustrating the impact of actions that fall short of maintaining the currency’s historical value. Understanding this analogy encourages reflection on the need for careful economic stewardship, timeliness in decision-making, and preserving a currency’s purchasing power to avoid regrettable outcomes.

A Day Late and a Dollar Short: Exploring Dollar Bearishness Across Asset Classes

What do stock market bulls, bears, gold bugs, homeowners, and commodity speculators have in common? This is not a trick question. The answer is that all these people are betting that the dollar will purchase less in the future than it does today. In other words, they are all dollar bears. Ask almost any stock, commodity or real estate bull about the end of their favourite asset class, and they will invariably say that their assets are appreciating in dollar terms. Part of this series can be accessed here: Day Late and a Dollar Short: Lessons in Timing and Consequence.

This is the same thing as saying the dollar is declining relative to that asset. Goldbugs and stock market bears claim that the dollar is dead and, therefore, only liquid tangible assets will have value in the future. Cash in US Dollars is possibly the most hated asset class around. Dollar bulls are as rare as dodo birds. Dollar bearishness seems reasonable considering the long history of dollar inflation and the reckless monetary policies of the US government. But we are contrarians, and when we see so many people on one side of the trade, we must analyze the consequences of such a lopsided market.

Unveiling the Looming Crisis: The Impending Peril of Dollar Scarcity

We feel that the extreme level of US dollar-denominated debt is at an inflexion point. Dollar debt is functionally similar to a dollar short position. Those who have borrowed money to exchange for another asset, believing that the other asset will appreciate in dollar value, have taken out the equivalent of a short sale of the dollar. Massive short sales have characteristics and consequences in markets, and these characteristics follow patterns. A crisis is dead ahead if the US dollar follows these same patterns. This will not be a crisis of dollar collapse but one of dollar scarcity. Few investors are prepared for such an event.

Most investors are positioned to profit from a declining dollar and would be devastated if the reverse occurs. This analysis flies directly in the face of conventional wisdom and the best efforts of our monetary authorities to devalue the currency. A dollar debt crisis would be a classic deflationary event. Still, unlike other more gradual deflationary scenarios, we envision the possibility of a rapid rise in practical dollar value that is similar to the characteristics of a short squeeze. A rapid increase in the dollar value is something few are prepared for and, therefore, would hurt many people.

This essay may disturb many devoted readers as we challenge cherished beliefs. But we are contrarians, and that’s what we do. You have been warned, so let’s get started.

A Dollar Short: What is a Short Position?

Purchasing a stock is called going long in the jargon of the investment industry. An investor buys and sells a stock in the familiar long trade, hopefully for a profit. A short sale is the inverse of the long position. The stock is sold for cash and then bought back later, hopefully at a lower price and, therefore a profit. In other words, sell high, buy low. How can an investor sell a stock he or she does not own? Investment brokerages always carry an inventory of stocks as part of their assets. Brokerages are allowed to lend stock to short-sellers who then sell the stock into the markets with the understanding that the stock will be returned and returned to the broker at some time. Selling a stock short allows the investor to profit from a decline in stock price.

Other assets, such as bonds, commodities and currencies, can also be sold short. The process is the same. The security is borrowed from a broker and immediately sold into the market. The position is closed when the security is repurchased and returned to the broker.

The Intricacies of Short Sales: Debt and Repayment

Since a short sale requires using a borrowed asset, a temporary position is a debt that must be repaid. It is a debt that must be repaid in kind with the same borrowed asset. The debt created by a short sale is collateralized by the cash received from the asset’s sale. The broker must hold this cash which will ultimately be used to buy back the shorted security and close the position.

A short sale is a risky position for an investor. The asset that is sold short may not drop in price as expected. The price may rise without limit, causing massive losses for an investor. At some point, an investor with a losing short position will be forced out of the trade by choice or the broker, who must return the asset to inventory via the dreaded margin call. A margin call occurs when the cash collateral falls below a certain threshold, and either the investor must provide more cash or the position will be closed by the broker using what’s left of the investor’s cash.

A Dollar Short and Short Squeezes

One of the most significant risks in short selling is the possibility of a short squeeze where many investors with short positions in the same asset try to close their positions simultaneously. Since closing a temporary position requires purchasing the asset, many buy orders hit simultaneously, causing a significant price spike and further losses for the short-sellers. Short squeezes can generate spectacular rallies that sometimes lift prices hundreds of per cent in a very short time and cause devastation for those who are caught in temporary positions.

A short squeeze typically occurs in a stock or asset with poor fundamentals. Investors are quick to exploit poor prospects by selling short. This causes the total number of shares sold short, called the short interest, to rise. At some point, the short interest rises so high that there becomes a shortage of stock available to trade. The stock starts rising in price as a result, and as short-sellers move to close positions, the price rise accelerates into a buying frenzy as panicked short-sellers buy at any price to stem losses. The essential characteristic of a short squeeze is the speed of the move. Short squeezes usually occur over relatively brief periods, catching many investors off guard.

Short Sales: The Risky Path to Repaying Debts

It is important to note that short-squeeze rallies do not signify any improvement in the fundamentals or prospects for the underlying asset. This is a technical market event solely the result of traders’ actions. The weaker the fundamentals of the asset, the more likely a short squeeze rally will occur. Many short squeeze rallies occurred in fragile tech stocks in 2003 because of excessive short selling in these securities. Many people assumed that these rallies were the beginning of a new bull market, but the fundamentals have not improved for most of these stocks; only the stock price is higher.

Short squeezes can occur in any market that allows short-selling, including commodities, futures, bonds, and currencies. Each market has different rules for short selling, so the details may differ, but the process is the same.

Similarities and Differences Between Cash Debt and Short Positions

We have seen that a short sale creates a debt that requires repayment of the asset at some time in the future. A short seller of stock sells the stock for cash, which becomes the collateral for the stock loan. A cash debt in the form of a collateralized loan is similar but reversed. Money is borrowed and immediately traded for an asset that becomes the collateral for the cash loan, which must be paid back with cash at some time in the future. In this way, a cash loan is similar to a short currency sale. If the asset purchased with borrowed cash increases in cash value, then the transaction was profitable because the loan value is now less than the cash value of the investment.

In the case of a stock short sale, no payments are required to maintain the loan, although interest may accrue. All that is required of the borrower is that the security is returned to the broker at some time in the future. With cash debt, however, many different repayment options exist. A loan may have fixed interest payments with a balloon at the end of the term (such as a typical bond), or it may be amortized where the principal is paid back continuously during the life of the loan (mortgages and consumer debt), or it could be “zero-coupon” debt where the entire principal plus interest is payable at the end of the loan.

The Finite Supply of Stock: A Catalyst for Short Squeezes

Another difference between a stock short sale and cash debt is that there is a limited supply of stock to sell short. Stock can only be sold short if there is inventory to sell. Therefore the limiting factor for stock short interest and the typical cause of a short squeeze is the lack of available supply. However, because of our fractional reserve banking system, there is a virtually unlimited ability to create new dollar debt regardless of the actual quantity of reserve cash available. The limiting factor for debt is the capacity to make payments rather than the amount of cash in the system.

When a broker lends stock to a short seller, the broker (lender) controls the transaction. The broker has possession of the stock and the cash collateral. If the short sale goes wrong, the broker can close the transaction to prevent losses to the lender. The lender of a short-sale asset can almost always collect from the borrower, so it is in a powerful position to recover assets. Troubles with short sellers rarely cause any systemic risk to the markets.

The Fragile Nature of Cash Loans: Limited Control and Systemic Risk

In the case of a cash loan, however, the lender has very little control over the loan’s progress. The lender rarely has possession of the collateral and must rely on the borrower’s trustworthiness to make the loan good. If the loan goes wrong, the lender must proceed through an expensive and time-consuming collection process that may include the sale of relatively illiquid collateral. In the case of a cash loan, the lender is in a distinctly weak position to collect from a troubled borrower. Because of the inherently weak position of cash lenders, widespread defaults on cash loans can cause systemic risks to the whole economy.

Significant similarities and essential differences exist between a short sale and a collateralized cash debt. The universe of cash debt transactions is far more diverse than that of short-sellers, but it is also far more entrenched in the economy’s working. The big question is whether the mountain of cash debt denominated in US dollars could unwind quickly in a situation similar to a short squeeze. We will analyze the dollar debt and money supply structure to probe this question.

Debt and Money Supply

There is an essential relationship between debt and money supply. Essentially, most of what we call money is some form of debt. We hold “cash” in “money market funds” and bank accounts, which are short-term IOUs, in other words, debt. Inflationists hail the massive increase in the reported money supply as evidence of hyperinflationary forces at work. However, broad money supply measures such as M3 and MZM include money market funds and other forms of short-term debt. Indeed, more money in the system chasing a limited amount of goods will cause general prices to rise.

Through the same process, more credit in the system will cause prices to rise. The problem with using credit as money is that it must be paid back. Credit that is paid back disappears out of circulation and is equivalent to a reduction in the money supply. Credit that is defaulted on takes even more additional credit out of the system due to a multiplier factor. This is the difference between cash and credit money. Cash stays in circulation, but credit money can be extinguished quickly. Less money in circulation, whether cash or credit, will cause a cash scarcity and ultimately lower general prices, i.e. deflation.

The Impact of the Stock Market Bubble: A Massive Surge in M3 Money Supply

The chart of the M3 money supply below shows a massive increase since 1995 when the stock market bubble took off. Since mid-2003, the chart has shown unusual volatility and may foretell a possible trend change. The unprecedented drop in the “M”s during the second half of 2003 is still unexplained but shows that even long-standing trends in money supply can change quickly without overt action from the central bank.

So, who is taking out this debt? The US Federal Government is responsible for a good portion of it, but they are in the enviable position of creating money from nothing. The US consumer owes the lion’s share of debt through the mortgage system. With all due respect to Joe Sixpack, we must conclude that the consumer is the dumb money. The average consumer has prepared for a crisis by racking up unprecedented debt during an economic slowdown.

Overwhelmed by Debt: Insufficient Income Growth and the Credit Machine

There is insufficient income growth to manage the increased debt service load. People should know they are over their heads but refuse to act responsibly and slow down the credit machine.

Why are they doing it? We think that this is one of the great questions of our time. The source seems more sociological than economic, and several undercurrents may exist. One possibility is that the events of 9/11 inspired a “live for today” mentality, with lenders all too willing to cooperate. Another option is that many people feel that they will ultimately be forced into bankruptcy anyway, so they might as well live it up until then and stick the lender with the bill.

The popular media has glorified gluttony and self-indulgence to the point that these are considered virtues. Excess is in, and frugality is out. Our waistlines are expanding as rapidly as our debt loads. There is some precedent for this social trend. In the late 1980s, the Japanese acted eerily similar to Americans today. We know how that ended.

Glorifying Excess: Media Influence and the Shift Away from Frugality

So, who is the smart money, and what are they doing? The charts above show that US businesses (smart money) are paying down debt. Commercial and Industrial loans have been falling since the end of 2000. It looks like smart money once again bailed out before dumb money.

They started cutting back on loans in 2000, while consumers waited till 2001. What is remarkable is first, the consumer never cut back as much as the business did. Secondly, even though they cut back, the ratio of consumer instalment credit to personal income has gone from dangerous to insane levels.

This is not sustainable; sooner or later, the consumer will say I can’t take it anymore, stop borrowing new money, and attempt to pay off their existing loans. This will buoy the US dollar as it will effectively be a short squeeze.

Unveiling Market Trends: Commercial Paper and Consumer Market Dynamics

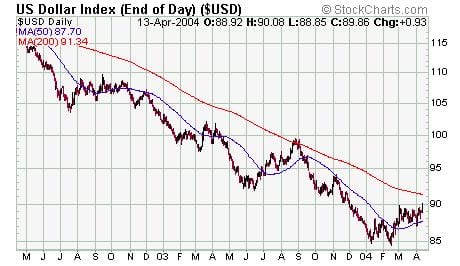

It is interesting to note that the commercial paper market topped the consumer market. The retail paper market topped just before the markets started to tank, and around the same time, the Dollar was topping. If one looks carefully now, they are trying to put in a bottom formation, which seems to coincide with the current bottom formation the dollar is putting in. Could these markets see something that most of us are missing?

Many readers wonder how we explain the sharp commodity rise regarding our call on the dollar. Commodities, particularly metals, performed spectacularly in 2003. To many observers, this is an indication of inflation and economic recovery. We disagree. The rally was ignited by weakness in the dollar and then fueled by misleading signals of recovery indicated by a sharp rise in GDP late in 2003. We believe that the GDP growth figures of 2003 are the direct result of massive stimulation from the government and also due to the depreciating dollar.

A Looming Reversal: Speculation, Hoarding, and the Potential Impact on Commodity Prices

These conditions are not likely to last much longer. The rise in commodities went parabolic in early 2004 and now seems to be sustained by speculation and hoarding. As of this writing, the entire metals complex is making a sharp correction coincident with a sharp rise in the dollar index. Although not yet indicating a trend change, this action supports our belief that a rising dollar will reverse the commodities rally. The rise in commodity prices may trigger a recession and cause its reversal.

What Would Happen In A Dollar Short Squeeze?

A dollar short squeeze would functionally resemble a general deflation but could unfold much faster. Deflation is a relative scarcity of cash and credit that causes a general price decline in a wide range of products, services, and assets. In other words, money becomes more valuable during a deflation. It would be triggered by some event that sucks enough liquidity out of the system to cause a chain reaction and serial debt defaults. A recession almost always accompanies deflation. The deeper the deflation, the deeper the recession.

The Dollar’s Paradox: Asset Appreciation and the Weak Dollar Effect

This is a scary scenario that few people see as a risk factor. In fact, in 2003, we witnessed the opposite effect as almost every asset class went up in dollar terms due to a weak dollar. There were several reasons for this, but it was primarily the result of a vast increase in credit chasing almost every product and asset insight. In essence, this was the effect of many people and investors going short the dollar by putting more credit into circulation and using it to buy stuff.

We seem to have inflationary expectations, which usually take time to work out. However, there have been several historical instances where a quick deflation followed sharp price inflation. In 1921 and in 1949, the US experienced a sudden deflation after several years of double-digit inflation. This shows that inflationary expectations, and by extension, the dollar, can turn on a dime (pardon the pun).

http://minneapolisfed.org/research/data/us/calc/hist1913.cfm

We envision several possible triggers for a dollar short squeeze. Here are just some of the more obvious ones:

Sudden interest rate rise.

This would cause an immediate slowdown in the housing market and cause highly leveraged speculators with variable-rate debt to liquidate immediately. Such a selling panic would feed upon itself. (As we wrote, long-term interest rates made a historic jump.)

Real estate bust.

The last real estate bust destroyed the entire S&L industry. This is one of the most potent risk factors for a liquidity crisis.

Debt saturation.

Debtors simply cannot assume more payment loads and attempt to pay down. This causes a decline in economic activity and money supply.

Tighter credit standards.

Credit standards are now the loosest in history. Almost anybody can get access to credit regardless of past or capacity. High default rates may cause lenders to tighten standards functionally, similar to a rate increase, since it would dramatically slow credit growth.

Supply shock.

A sharp price increase in essential commodities such as energy or food acts as a tax on discretionary income, diverting it to non-discretionary items and causing a recession. It also hits businesses with high commodity input costs but limited pricing power. This happened in the 1970s during the oil shocks and caused an inflationary recession. However, with the current global labour arbitrage situation and low capacity utilization for industry, prices for many goods could fall and cause a net deflation.

Derivative meltdown.

Most of the $150+ Trillion in derivatives worldwide are interest rate related. A sudden, unexpected change, either up or down, may cause counterparty failures and a liquidity crunch. This happened once in 1998 by a single firm that almost broke the global financial system.

Contingent debt.

Much commercial debt is contracted on a continent basis by tying it to the market value of collateral such as stocks or real estate. This debt becomes callable if the market value of the collateral drops below a certain level. This is what brought down Enron and some other energy companies in 2001. It is difficult to quantify this risk because the contingent debt market is private and highly opaque. A large default in contingent debt could cause a domino effect and trigger a liquidity crunch.

Terrorism.

Utterly unpredictable in scale and impact but a specific risk factor.

Asset market correction.

Many people take their economic cues from the stock and bond markets under the assumption that they foretell the future. A sharp drop in the stock markets, for example, has been known to cause consumption to fall because of the ‘wealth effect’, leading to recession.

In the aftermath of such an event, the dollar would likely resume its decline due to the continued deterioration of the fundamentals of the US economy. Remember, a short squeeze indicates no change in asset or security fundamentals. It is a confirmation of its weakness. The irony of the situation is that those who are convinced that the dollar is slowly dying are probably right, but their collective action makes their investment positions untenable.

Official Countermeasures

We can assume that the government and other authorities would fight tooth and nail deflation. They have pulled out all of the stops since 2000 with hyperinflationary fiscal and monetary policies. However, the government has often usurped even more power and authority in past deflations. The greatest increases in US federal government authority occurred during the Great Depression. Although a sitting administration would almost certainly be blamed for such an economic calamity, entrenched government bureaucrats may thwart the senior authorities’ efforts to expand their influence during the crisis.

Here are some possible countermeasures:

Fiscal and monetary policy.

Most of the bullets have already been used. There is little room for monetary policy, and further fiscal stimulus would be politically untenable if they increase the deficit.

Helicopter money.

Throwing money out of helicopters would cause chaos. Of course, I am just joking, but this might be possible if things go out of hand. The method most likely to be employed would be to find some excuse to issue more tax rebates, but this takes time. Even if the banks were to put money directly into the individual’s accounts, this still might not be fast enough. First, no one can guarantee that the consumer will take that money and spend it. If they suddenly feel things will get significantly worse, they might hoard that money, further aggravating the problem.

Bailouts.

Politically explosive if the bailouts are for large institutions. Small bailouts would be administratively bogged down due to the sheer number.

Market holidays.

It seems like a shot in the dark, as it would only delay the inevitable and not alter much. The real problem would not disappear.

Payment moratoriums.

This could have the opposite desired effect, and now the whole world would see that there is indeed a severe problem for such drastic measures to be implemented. This could have the effect of effectively stemming all future expenditures.

Most official responses to a sudden deflation would be ineffective and bogged down in administrative delay. The Federal Reserve has the tools and authority to reflate the banking system. However, most debt creation these days is outside the banking system, and the Fed could not efficiently respond in the case of widespread default.

Winners and Losers

Stocks

will most likely lose as the current market rise has simply been inflationary, whereby the Dow and Nasdaq simply readjusted to reflect the dying dollar. We illustrated this point last year when we priced the Dow in Several strong currencies, the strongest at that time being the Rand. The Dow had done virtually nothing when viewed in terms of stronger currencies. So it is possible that a rising dollar could hurt stocks as the market now readjusts downwards to consider the deflationary forces. This most likely will not happen immediately as one still has to consider the mass psychological components. Individuals once again have become accustomed to buying the dip. So after this current correction, we could rally one more time before we take a massive hit, and the markets are now allowed to price in all the possible deflationary forces.

Commodities.

Gold, Silver and Platinum will probably correct hard initially, but this will be a short-term aberration and will most likely provide an excellent opportunity to take new positions. The other commodities, such as aluminium, copper, tin etc., will most likely take a big hit as economies worldwide start to slow down and deflationary forces exert their full strength.

Land and housing.

This is where the most significant risk factor lies. The housing market has entered a bubble stage; anyone with a pulse can apply and get a mortgage. Individuals who have no right to buy houses are now buying homes because they are made to believe it’s a good investment with almost no risk involved. I have noticed ads all over the place portraying the landlord as a greedy, despicable person getting rich on rent.

This story is entirely overrated. I have looked at the housing prices in New York, and at current prices, it does not make sense to be a landlord as the rent barely pays the inflated mortgages. So one must conclude that people still keep buying because they think houses will keep going up forever. Whenever the masses thought they had found the next Holy Grail, disaster loomed around the corner, waiting to rear its ugly head.

So, in conclusion, both land and housing will get hit very hard simply because they have both been in an overextended speculative bubble and once the consumer stops spending, let’s forget about savings for the time being. If they start to cut down on their debt levels by not taking new debt and paying off the existing debt, the housing market and the economy will come to a sliding halt.

Bonds.

Sovereign bonds such as US Treasuries and the issues of other federal governments usually rise as interest rates continue to fall during a deflation. Corporate bonds, mortgage bonds, and other asset-backed instruments may do poorly if defaults are widespread.

Bank deposits.

All banks within the US are covered by deposit insurance and, more importantly, have direct access to the Federal Reserve printing press. Even massive problems in the banking system can be handled within the existing structure. The S&L crisis was handled well and resulted in almost no severe losses for depositors.

Money market funds.

If the funds are invested in US Treasury bills, then there is no risk of default, but many funds buy much riskier paper to boost yields. All money market funds should be 100% US Treasury. There is little to be gained by taking on extra risk trying to grab an extra ½% yield.

Tips.

Much noise is being made about TIPs: investing in bonds with an inflation hedge. The problem here is assuming that inflation will be the only problem. If deflationary forces take over, those who invest in this area could take a beating.

Other Voices

We are not the only analysts to voice these opinions. Several other noted authorities have discussed the possibility of a dollar short squeeze in various contexts.

Bob Hoye from Institutional Advisors states:

“The world has experienced the biggest financial boom in history, including the biggest debt issuance in recorded history. And the majority of this in “street” terms is equivalent to a huge short position in the senior currency. The eventual problems in servicing debt, which in the world of traders can be construed as “short-covering”, in the past became intolerable.”

http://www.gold-eagle.com/editorials_04/hoye040604.html

Rick Ackerman’s Perspective: Short Squeeze and the Dollar Bear Market

“In a financial crisis, might the unwillingness of lenders to roll short-term paper create a short-squeeze demand for cash dollars? Maybe. But the spike would be so precipitous as to be unsustainable, and that implies the dollar could only collapse back into itself once the squeeze had subsided.”

http://www.rickackerman.com/41.html

Did you know that most mortgages are contingent loans? BEI of Oregon shows how even homeowners in good standing can face foreclosure:

“Because most home loans have clauses to the effect that the lender may, at its option, call the loan due in full if the collateral value falls to a point they believe puts the loan in danger. The bottom line? Even if you never miss a payment and are ahead of schedule, if your collateral falls in value, your home may well be foreclosed by the lender.”

http://www.beioforegon.com/newsletters/specialreports/200110.htm

On the issue of the inflationary impact of rising commodity prices, Van Hoisington reminds us that:

“The unhappy fact is that rising prices of commodities, gasoline, medical care, food, and other non-discretionary items that people buy without increasing income is not inflationary, but disinflationary. Essentially, the hike in necessities acts as a tax in an income-constrained environment. Income growth in excess of price changes is critical to getting the inflation ball rolling, and that simply is not happening.”

http://www.hoisingtonmgt.com/HIM2004Q1NP.pdf

~ CONCLUSIONS ~

This is probably the most challenging essay I’ve ever written. Partly it is because of the difficulty of the subject matter, but primarily because of the disturbing conclusion I must make. As a child, I was taught to say nothing if I didn’t have anything good to say, and I’m afraid I don’t have anything good to say due to this analysis. A dollar crisis in the form of a short squeeze would be devastating to millions of people and to the global economy. Paradoxically, a short sharp rally in the US dollar may further weaken the already creaky US economy by collapsing exports.

Investors and consumers seem to have an almost religious belief in the ability of the Federal Reserve to handle any potential liquidity crisis. Indeed, they have been extraordinarily successful at handling crises such as LTCM and the S&L debacle. However the scope of these crises was limited, and this was when the banking system still had control of most credit creation. This has changed, and now most of the credit creation is outside the banking system, where the Fed has only marginal influence. I think the monetary authorities are acutely aware of this, and their policies reflect extreme concern.

As we wrote this essay, the dollar rose sharply, interest rates spiked, and stocks and commodities fell. This may only be a temporary trend, but it seems to follow our described pattern. I hope this analysis is wrong because I don’t want to see people hurt, but even if it is partly valid, investors must prepare for such an event.

Prudent Measures: Insurance Against Deflation and Planning for Different Scenarios

The most helpful preparation any investor can make is getting out of debt. This is good advice in any event, but particularly now. Other practices can include the purchase of some gold and silver coins or bullion and having an adequate supply of paper cash in the form of a selection of national currencies, including US dollars. Robert Prechter’s book Conquer The Crash recommends sensible and appropriate defences against rapid deflation. These are not radical suggestions and do not preclude investors from playing the inflation trade simultaneously via non-leveraged stock and commodity investments. Preparations for deflation are typically conservative and straightforward.

The scenarios outlined in this essay may or may not come to pass, but I feel strongly that they have a definite possibility of occurring. Taking out some insurance against deflation is prudent, even if the opportunity seems remote. We take out insurance against many unlikely events and think nothing of it. Prepare for the worst, but plan for the best.

George J. Paulos

Editor/Publisher

Freebuck.com – Alternatives for Financial Freedom

http://www.freebuck.com

Email

Sol’s Conclusions

Many people have written on this subject recently, though not in such detail. However, George approached me with this idea last year. At that time, no one ever broached the topic. So, while George may not have put his thoughts to paper as fast, I had some part to play in the delay as I did not jump on his idea immediately. I think he was the first to see the adverse effects of our current debt levels and, in my opinion, was the first to point out that this insane level of debt could be viewed as a short position against the dollar.

I also agree with him in that this is perhaps the most challenging and complex topic I have ever had to deal with and probably will be the most difficult one for a while. There are so many possibilities that it is hard to predict how dire the situation will be once the House of Cards starts to crash. There is no doubt that the situation is eventually going to be terrible. The question is just to what degree.

Contrarian Investor Strategies and the Importance of Debt Reduction

All wise contrarian investors should significantly reduce their debt levels and stop taking on new debt. In addition, one should have some money parked in Gold and Silver Bullion. If you have no positions in either, take recent posts on any significant major pullback.

Credit facilities are being extended to anyone who can breathe. All you need to do regarding mortgages is have a pulse and scratch your name on the signature line. They have mortgages for every category: those with not-so-good credit, those with terrible credit, and even those with bankruptcies can get a loan now, and just a few years ago, they came up with the ultimate mortgage, a “no income verification mortgage.” Recently, I found out that an even more insane mortgage exists. It’s called a complete no-document mortgage. One only needs to come up with 5-10% of the down payment, depending on your credit and voila, you are now a proud Slave. I cannot call anyone a proud owner unless they buy these houses in a few select areas of the US where housing prices are still somewhat sane.

The Death Mortgage: Extending the Burden with 40-Year Mortgages

Just recently, they have introduced what I call the Death mortgage, the so-called 40-year mortgage. As if 30 years of tying your neck around a rope is not enough, they find a way to enslave you for ten more years. This mortgage is being touted as the solution for new buyers to compensate for the increased prices of houses. So now you can still buy that 500k house and have monthly payments that fit your budget. Insane offers usually come right towards the last stage of a bubble. The 40-year mortgage certainly qualifies as one. You can click on one of the three links below for those interested in details. (Ed. note: 100-year mortgages are often taken out in Japan. Nice gift to the grandchildren.)

http://www.startmymortgage.com/Mortgage_Types/40-year_mortgages.htm

http://www.bankrate.com/brm/news/mtg/20000316.asp

http://www.detnews.com/2002/realestate/0207/18/g03-535119.htm

The Uncertainty of the US Consumer

The actual wild card in this situation is the US consumer. How is he going to react? Subtitle 1: The Uncertainty of the US Consumer.

I noticed that Yahoo! had a top story stating that US consumers are nervous about buying new houses because of rising property taxes. How nervous will they get if the housing market suddenly starts crumbling? Imagine a 50% drop in sales of new homes; this would blow the last legs of this market. Or, for that matter, let’s say they stopped taking new loans from banks to buy cars they did not need or appliances that were not necessary or purchasing a second home for investment purposes taking out home equity loans to buy stocks or bullion, and the list goes on.

The Dilemma of Cash in Deflationary Times: Challenges of Liquidating Bullion

The scary thing in a deflationary situation is that cash is usually hard to come by. So, let’s assume you want to cash in some of the enormous profits you have in bullion, so you go to your local bullion house only to be told they have no cash on hand. Stop to think for a second. It would help if you still had paper cash to buy things. People don’t use gold coins or gold bars to pay for groceries; even if they want to, the system is not yet set up. For those of you who might think that we are getting negative on Gold and Silver, look at our comments once more under commodities. We don’t believe the general long-term trend will be broken, but that does not mean a significant correction is not a strong possibility.

The Fragile Foundation of the Economy

This whole economy is built on credit. This so-called economic era of huge gains is nothing but a lie. This significant era of so-called prosperity is an illusion without taking on new debt. We are sitting on a glasshouse, and the first hairline cracks have appeared. The transition from all to nothing will be so fast that most won’t even know what hit them when this happens. Subtitle 2: The Fragile Foundations of the Economy.

The rise of the dollar could be the tip of the iceberg, but remember, it could also be the tip that you need to get your house in order. Debt will become a foul word, and savings will be treasured again. The only variable is time. It’s not about whether or not it will happen but when.

Sol Palha

Tactical Investor

http://www.tacticalinvestor.com

Acknowledgement

The sunset graphic is the artwork of Paul J. Heslin. View more of his work at who3d

Originally published on April 15, 2004, this piece has undergone several updates, with the latest update in October 2023.

FAQ – Dollar Short Squeeze and Deflation Risks

Q: What is a dollar short squeeze?

A: A dollar short squeeze refers to a situation where there is a relative scarcity of cash and credit, causing a general decline in prices of products, services, and assets. It can unfold rapidly and be triggered by an event that removes liquidity from the system, leading to chain reactions and debt defaults.

Q: How does a dollar short squeeze relate to deflation?

A: A dollar short squeeze resembles a form of deflation, which is a general decline in prices. During deflation, money becomes more valuable. A dollar short squeeze can exacerbate deflationary pressures and lead to a deeper recession.

Q: What are the triggers for a dollar short squeeze?

A: Some potential triggers for a dollar short squeeze include sudden interest rate rises, a real estate bust, debt saturation, tighter credit standards, supply shocks (such as sharp price increases in essential commodities), derivative meltdowns, contingent debt defaults,, and terrorism.

Q: What countermeasures can be taken to combat deflation?

A: In response to deflation, various countermeasures can be employed, including fiscal and monetary policies, helicopter money (direct distribution of money to individuals), bailouts (although politically challenging), market holidays (temporary closure of financial markets), and payment moratoriums (temporary suspension of payments). However, many official responses may be ineffective or delayed.

Q: What assets are likely to be affected in a deflationary scenario?

A: In a deflationary scenario, stocks may face losses, commodities may experience initial corrections but could present investment opportunities, land and housing markets may suffer significant declines due to overextended speculative bubbles, sovereign bonds may rise while corporate and asset-backed bonds may perform poorly, and bank deposits may generally be protected but can be impacted if widespread defaults occur.

Q: Are any notable experts discussing the risk of a dollar short squeeze?

A: Several experts have raised concerns about the possibility of a dollar short squeeze. Bob Hoye from Institutional Advisors, Rick Ackerman, and BEI of Oregon are among those who have highlighted the potential risks.

Q: How can individuals prepare for a deflationary scenario?

A: Prudent measures to prepare for deflation include reducing debt, diversifying holdings to include gold and silver coins or bullion, holding an adequate supply of paper cash in different national currencies, and considering conservative investment strategies. It is recommended to have a plan that accounts for different scenarios and balances the potential risks of deflation and inflation.

Expand Your Mind: A Selection of Intriguing Articles