The Great Investment Rush: Understanding the 1920s Stock Market Phenomenon

Oct 23, 2024

It’s 1920, and a shoe-shine boy eagerly offers stock tips alongside his polish service… this scene, famously recalled by Jesse Livermore, became a defining symbol of the era’s unprecedented stock market mania. The “1920s roaring twenties” marked a transformative period in American financial history, where Main Street met Wall Street in an explosive confluence of opportunity, innovation, and, ultimately, devastating speculation.

The Perfect Storm: Economic Factors Driving Market Participation

The post-World War I economic boom created a unique environment that drew investors to the stock market like never before. Consumer confidence soared as new technologies – automobiles, radios, and household appliances – revolutionized daily life. As Benjamin Graham noted, “The market is not a weighing machine, but a voting machine.” This observation proved particularly prescient during the 1920s, when public sentiment, rather than fundamental value, increasingly drove stock prices.

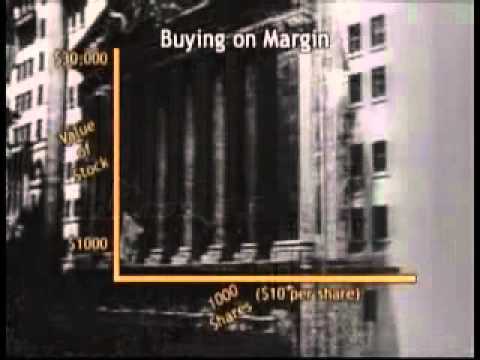

Manufacturing efficiency reached new heights, wages increased, and Americans found themselves with disposable income and an appetite for investment. The introduction of buying stocks “on margin” – purchasing shares with borrowed money – made market participation accessible to the middle class, though this practice would later contribute to the market’s downfall.

Mass Psychology and Market Momentum

John Templeton, renowned for his contrarian investment philosophy, often emphasized how extreme market conditions arise from mass psychological factors. During the “1920s roaring twenties,” several psychological elements converged to create what we now recognize as a classic bubble:

1. The “new era” thinking that suggested traditional valuation metrics no longer applied

2. The fear of missing out (FOMO) that drove even conservative investors into speculative positions

3. The widespread belief that stocks could only go up

4. The emergence of celebrity investors and market gurus

As more investors entered the market and saw quick profits, their success stories attracted others, creating a self-reinforcing cycle of investment and speculation.

Innovation and Speculation: The Double-Edged Sword

Warren Buffett often remarks that innovation and investment success don’t necessarily go hand in hand. The 1920s proved this point dramatically. While genuine technological breakthroughs drove initial market gains, speculation soon overtook innovation as the primary market driver. The period saw the birth of investment trusts – similar to modern mutual funds – which promised professional management and diversification but often engaged in dangerous levels of leverage and speculation.

Radio Corporation of America (RCA) became the era’s darling stock, rising from $1.50 per share in 1921 to $573 in 1929. This spectacular rise exemplified both the period’s potential and its peril.

The story of RCA perfectly encapsulates the era’s marriage of innovation and speculation. Founded in 1919, RCA revolutionized communications through radio technology, much like how the internet transformed our world decades later. The company’s innovative achievements were genuine: it established the first radio network (NBC), developed improved vacuum tubes, and laid the groundwork for television technology. However, as Jesse Livermore observed, “Markets are never wrong – opinions often are.” The stock’s meteoric rise wasn’t solely based on technological progress but on widespread speculation about radio’s future potential.

Investment trusts, another innovation of the “1920s roaring twenties,” played a crucial role in amplifying market speculation. These vehicles, pioneered by financial entrepreneurs like Goldman Sachs Trading Corporation, created complex pyramids of leverage. A single trust might own shares in other trusts, which in turn owned shares in yet more trusts, creating a dangerous web of cross-ownership and hidden leverage. Benjamin Graham later described this structure as “a house of cards built on a foundation of sand.”

The innovation frenzy extended beyond radio and finance. Automobile stocks like General Motors saw their values soar as car ownership became widespread. Aviation stocks captured investors’ imaginations despite most aircraft companies being unprofitable. New electrical appliance manufacturers promised to revolutionize home life, leading to frenzied buying of their shares. The pattern was consistent: legitimate technological progress sparked investment interest, which then morphed into pure speculation disconnected from business fundamentals.

The era’s newspaper headlines tell the story vividly. “Radio Stock Soars Again!” declared the New York Times in 1928. “New Era of Permanent Prosperity!” proclaimed the Wall Street Journal. These headlines eerily echo modern cryptocurrency and tech stock coverage, demonstrating how little has changed in market psychology over a century.

The period also saw the emergence of celebrity investors and market manipulators. Figures like William Durant, who founded General Motors, became household names through their market activities. Their success stories fueled public conviction that anyone could get rich through stock speculation. This democratization of investment opportunity, while potentially positive, led to dangerous levels of market participation by inexperienced investors.

As George Soros later theorised, these dynamics created a “reflexive” relationship between innovation and speculation. Real technological progress justified initial price increases, which attracted speculators. Their buying pushed prices higher, validating the original investment thesis and attracting more buyers in a self-reinforcing cycle. This pattern repeated across multiple sectors, creating what economic historians now recognize as one of history’s most dramatic market bubbles.

The Role of Credit and Leverage

George Soros’s theory of reflexivity – where market perceptions create self-reinforcing cycles – helps explain how credit expansion fueled the 1920s bubble. By 1928, brokers’ loans had reached $6 billion, nearly double the amount from just three years earlier. This easy credit created a dangerous feedback loop:

– Rising stock prices encouraged more borrowing

– More borrowing led to more stock purchases

– More purchases drove prices higher still

– Higher prices justified even more borrowing

The Federal Reserve recognized the dangers but proved reluctant to take decisive action, fearing economic disruption.

Cultural Transformation and Market Participation

The democratization of stock market investing during the “1920s roaring twenties” represented a profound cultural shift. As Jesse Livermore observed, “The average man doesn’t wish to be told that it is a bull or bear market. He desires to be told specifically which stock to buy or sell. He wants to get something for nothing. He does not wish to work. He doesn’t even wish to have to think.”

This observation captures the era’s transformation of stock market participation from a sophisticated pursuit of the wealthy into a national pastime. Newspapers expanded their financial sections, and investment clubs sprouted across the country.

The Warning Signs and Missed Signals

Benjamin Graham’s emphasis on fundamental analysis and margin of safety starkly contrasted the period’s speculative excess. Several warning signs emerged:

1. Price-to-earnings ratios reached unprecedented levels

2. Corporate insiders began selling their holdings

3. Economic indicators showed signs of weakness

4. Market volatility increased significantly

Yet most investors, caught up in the euphoria, ignored these signals. The parallel to modern market cycles is striking, demonstrating how little human nature has changed over the centuries.

Lessons for Modern Investors

The “1920s roaring twenties” stock market boom offers crucial lessons for today’s investors. As Warren Buffett famously said, “Be fearful when others are greedy, and greedy when others are fearful.” This period demonstrates why:

1. Speculation can persist longer than expected

2. Leverage amplifies both gains and losses

3. Popular sentiment often overwhelms fundamental analysis

4. Innovation doesn’t guarantee investment success

5. Market psychology drives short-term price movements

The era’s eventual collapse reinforces the importance of maintaining a margin of safety and avoiding excessive leverage.

Conclusion: The Eternal Cycle

The stock market boom of the “1920s roaring twenties” remains a compelling case study in market psychology, speculation, and the consequences of unchecked optimism. While the specific circumstances of that era may never repeat exactly, the underlying patterns of human behaviour continue to influence markets today. Understanding this history helps modern investors recognize similar patterns and maintain perspective during periods of market euphoria or panic.

The lesson isn’t to avoid market participation entirely but to approach it with wisdom, understanding, and respect for fundamental principles. As John Templeton observed, “The four most dangerous words in investing are: ‘This time it’s different.'” The 1920s proved this maxim true, and it remains equally relevant for investors today.