Introduction

Jan 14, 2025

How often do we see share prices skyrocket because of widespread excitement, only for investors to spiral into panic once the bubble bursts? This cycle, familiar to many, has a dramatic low point sometimes referred to as the “valley of despair.” Imagine an enthusiastic crowd chanting ever louder about a particular stock or sector, convinced that the uptrend would never end. Suddenly, signs of trouble emerge, sending traders scurrying to sell everything at once, leaving share values in tatters. This whiplash highlights a truth long recognised by market veterans: no rally lasts forever, and no decline is truly endless. Our goal here is to explore the path from euphoria to despair and back again, drawing upon psychology, technical signals, and some of history’s most sobering examples.

Consider how major manias, like the dot-com bubble of the late 1990s, enthralled even cautious individuals. Start-up firms with limited earnings soared purely on hype. Then, almost overnight, the air came rushing out, plunging speculators into a deep well of regret. Those who viewed the spike with scepticism often fared better than those who preferred blind optimism. Similarly, the 2008 housing debacle reminded everyone that property can crash, even if pundits claim it never will. Prices climbed on the back of generous lending and overconfidence, culminating in a heart-stopping collapse once mortgage defaults started rising.

The emotional escalator that leads from the dawn of hope to the valley of despair gives us a bird’s-eye look at how mass behaviour can distort logic. This essay sheds light on how fear and elation interact with technical methods to repeatedly create the booms and busts we observe. By weaving real-world anecdotes with ideas from finance and psychology, we will see not merely how these cycles repeat, but how the anticipation of dramatic shifts can set astute investors apart from the panic-driven majority. In doing so, we challenge the notion that the best plan is to follow the crowd. Instead, the discussion will suggest how being rational at precisely those moments when others lose their cool can turn a potential catastrophe into a golden opportunity.

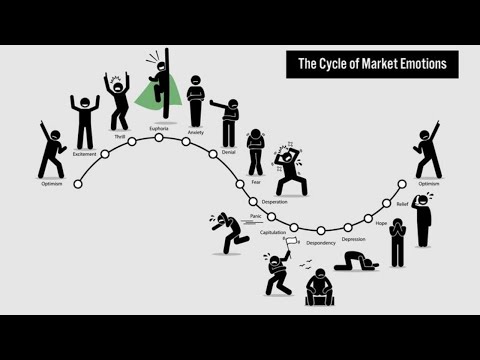

The “Valley of Despair” in Market Cycles

The phrase “valley of despair” pictures a bleak pit on an emotional roller coaster. In financial terms, it describes the stage at which investors have endured such brutal declines that many abandon hope. They can no longer imagine a recovery, having seen what began as a promising investment unravel before their eyes. Whether prompted by bursting tech bubbles or housing meltdowns, the story remains the same: participants are so shaken that they sell en masse, cementing their losses and missing potential rebounds. From a psychological standpoint, this is the capitulation phase, where despair outweighs all else, convincing some that it is best to exit completely.

Many compare this phenomenon to the “Wall Street Cheat Sheet,” a popular depiction of how market sentiment travels from optimism through excitement to euphoria, only to reverse toward anxiety, denial, and, finally, despondency. Once certain leading shares have collapsed, and news outlets report wave after wave of financial distress, it is tempting to assume that the slide will continue indefinitely. Pessimism becomes overwhelming, overshadowing any small signs of improvement. Yet, historically, markets often find some form of bottom at these low points, setting the stage for a future upswing.

The valley of despair is not limited to stocks. It can happen in commodity markets, such as when oil prices cratered in the mid-2010s or in real estate, as seen in the late 2000s. Regardless of the instrument, the emotional undercurrent is comparable. A crowd that once inflated prices now becomes convinced there is no floor. At that very moment, patients with a contrarian spirit might see an entry opportunity, provided they base their decisions on tangible data and not just blind hope. Indeed, time and again, the greatest gains appear once the market has punished everyone who got carried away during the previous euphoria. The crucial factor is having the fortitude and groundwork to act at the point of peak gloom.

Ill-informed panic selling often happens because individuals focus on short-term headlines instead of broader trends. People see daily plunges rather than weighing overall value. Despondency can push investors to forget that recoveries do occur. Left unchecked, it dismantles reason, handing over control to fear. Learning to recognise this downward spiral lays the groundwork for a steadier hand, particularly for those who train themselves to treat a market meltdown as a potential bargain hunt rather than the end of stability.

Mass Psychology: Fear and Euphoria

Financial markets mirror human emotions, shifting from confidence to dread with a tempo that can bewilder the uninitiated. When enthusiasm takes centre stage, investors may disregard valuations, blindly chasing the “next big thing.” This mania can raise prices sky-high, prompting the media to declare a new era of endless prosperity. During these hopeful times, caution is often ridiculed, while risk-taking on credit or margin is applauded. Only afterwards does it become clear that such breathless optimism was oversold once the inevitable tipping point strikes.

On the other hand, as events sour, the pendulum swings to the opposite extreme. Fear becomes more infectious than any disease, leading to indiscriminate selling and self-protective decisions that pile misery on an already battered market. Stories about bankruptcies and job cuts fill the news cycle, reinforcing the notion that assets may remain beaten down without bounds. This fear tends to become self-fulfilling, at least for a while, as liquidity dries up and demand melts.

In his famous writings, John Maynard Keynes noted that markets can stay irrational longer than most people can stay solvent. This observation applies equally to phases of confidence and despair. Overextended rallies persist partly because traders feel unstoppable in a rising climate, while slumps can go deeper than estimates because panic is hard to reverse once set in motion. Recognising that both euphoria and fear might reach excessive levels helps an investor avoid the traps set by misguided emotional swings. If, for instance, a share doubles on headlines of extraordinary potential but the underlying numbers do not match the hype, caution is warranted. Likewise, if a stock collapses and the gloom overshadowing it seems out of proportion to its fundamentals, it may be worth closer examination.

Such emotional extremes explain how bubbles germinate and why collapses can become brutal. Behind every chart or data point lies a mass of buyers and sellers governed by psychological biases and primal instincts. Dealing with these impulses requires self-awareness. Investors who break free from the crowd’s collective feelings stand a better chance of making level-headed moves. This is where the “valley of despair” can transform from a place of hopelessness for many into a fertile ground for measured, calculated buying for a few.

Behavioural Finance and Technical Analysis

The theories behind behavioural finance underscore that individuals often act in ways that defy logic. Cognitive biases, such as confirmation bias or loss aversion, shape decisions more than rational evaluation. During an upswing, confirmation bias encourages people to seek evidence supporting the notion of further gains, discarding contrary data. This feeds groupthink. Meanwhile, loss aversion intensifies fear during downturns, leading investors to lock in losses to avoid the possibility of deeper pain. Both phenomena contribute to exaggerated price moves and reinforce the cyclical nature of booms and busts.

Technical analysis emerges as one way to shed some light on market sentiment in a more structured manner. By examining price trends, volume patterns, or momentum indicators, traders can see whether the mania or despondency has pushed the market away from typical ranges. For instance, the Relative Strength Index (RSI) can reveal when a stock or index is overbought, hinting that enthusiasm might have run too far. Conversely, an oversold reading can signal that fear has reached an extreme. Although such signals are not guaranteed to pinpoint exact reversal moments, they often warn that the established trend appears unsustainable.

Another reliable tool is the Moving Average Convergence Divergence (MACD), which compares short-term and long-term moving averages to gauge momentum shifts. When the MACD crosses below a signal line amid bullish chatter, it might suggest that the rally is weakening. Conversely, if it crosses above the line after a pronounced sell-off, it can point to returning optimism. While neither RSI nor MACD replaces thorough research, they can help investors see potential market psychology imbalances. Such patterns have reappeared time after time, whether during the dot-com upswing or the subsequent tech crash and again in the property mania that preceded the 2008 financial crisis.

Of course, technical methods sometimes produce confusing signals, especially if the prevailing emotions overwhelm normal patterns. However, these tools still help guard against runaway euphoria or panic by providing objective data. A trader who notes that multiple indicators are flashing warnings can apply caution, perhaps selling part of a position or placing stop-loss orders. Conversely, when everything points to an overdone route, that same trader may add risk incrementally, guided by disciplined money management. In this manner, behavioural finance and technical analysis unite theory and practice, giving a measure of structure to an otherwise emotionally driven environment.

Strategic Buying and Securing Profits

A widely shared notion in stock markets is “buy low, sell high,” but this advice can be deceptively simple. The real challenge is to judge when prices are genuinely “low” or “high.” Panic-driven sell-offs can pull a quality asset down alongside weaker peers, creating bargains for the discerning eye. However, few have the courage to invest when news screams doom. This is precisely why strategic buying during crash conditions can, over time, generate impressive returns. Instead of taking flight at the first hint of trouble, certain investors do the opposite, quietly building stakes in solid companies whose share prices have collapsed due to the general sense of alarm. Such contrarian techniques hinge on bucking the natural urge to follow the crowd.

The flipside is equally relevant. During boom times, many refuse to sell, believing there could still be more upside. The dot-com bubble saw countless enthusiasts, reluctant to miss the next leg up, holding troublesome tech stocks. But paper profits are worthless if the subsequent crash wipes them out. Learning to trim positions or secure gains when the public mood is excessively optimistic remains a powerful tactic. This might involve scaling out in stages rather than selling everything at once. For instance, if a stock has doubled in value on the back of hype, taking some chips off the table can prevent a scenario where all those gains vanish overnight. Some market veterans advise at least recouping the initial investment, thus remaining in the position with “house money.”

A classic case is the run-up in real estate before 2008. Many property owners believed the surge could last for a decade or more, with few looking to lock in sizable gains. Yet the small minority who sold near the top and reinvested after the crash, once fear had peaked, often emerged in a stronger financial position. Timing is rarely perfect, but a balanced approach that includes partial profit-taking and selective entry during distressed periods can outperform the naive strategy of riding bubbles to their peak and suffering the subsequent decline. Experts often emphasise that while no one can predict exact tops or bottoms, staying alert to warning signs significantly boosts an investor’s odds of success.

Implementing a plan that outlines precise rules—such as how gains will be locked in, how new entries will be funded, and how position sizes will be managed—enables an investor to act calmly rather than emotionally. This approach reduces rash decisions prompted by the news cycle. The idea is to focus on what is probable rather than what is popular. Short-term fads can be exhilarating, but they can also end in tears if not treated with caution. In short, strategic buying goes hand in hand with strategic profit-taking. One is useless without the other.

Conclusion

Why does the journey from optimism to the valley of despair catch so many unawares, time after time? Part of the explanation rests with human nature itself. We enjoy good news and hope that sunshine will persist forever. At the same time, we recoil from warnings of danger, dismissing them as irrelevant or even inconvenient. Once the market begins to wobble, we pivot to panic, convinced that no light exists at the end of the tunnel. Real success belongs to those who recognise that these emotional extremes are woven into every bull and bear saga. We need not scurry along with the crowd nor be contrarian for its own sake, but we do well to approach the cycles with a structured plan.

The valley of despair should thus be viewed not as a dead end but as an occasion to reflect on how panic shapes opportunity. When a once-high-flying sector plummets, analysis might reveal that panic is overdone, creating a channel through which a shrewd investor can buy shares at discounted levels. Conversely, when everything is shining with too much promise, the prudent trader sees the risk of an overheated market, forging a plan to protect gains. Accepting that markets do not move in straight lines can be liberating because it admits the utility of basic checks and balances, whether employing technical indicators or evaluating the fundamental qualities of a company.

Real-world episodes like the dot-com and housing crises confirm that the pendulum swings widely, with emotions amplifying each move. Those who plan for these extremes, whether by selling in stages near peak confidence or entering selectively during waves of despair, place themselves on stronger footing than the herd. No method is guaranteed to be flawless, and timing exact tops or bottoms is notoriously difficult. Yet, the patterns laid bare by behavioural research and chart signals give us enough clues to avoid the worst mistakes. In a realm so prone to hype and hysteria, a cool head—armed with deliberate techniques for both entry and exit—remains an investor’s most dependable asset. This mindset transforms the valley of despair from a forbidding trap into a possible gateway to future success.