May 28, 2026

In theory, policymakers can absolutely try to recreate some version of the post-2008 liquidity system. The Federal Reserve can create reserves again, the Treasury can issue enormous quantities of debt again, and banks can still absorb Treasuries if conditions allow. Operationally, none of that is especially mysterious. Central banks understand the mechanics very well because they already ran the experiment for more than a decade.

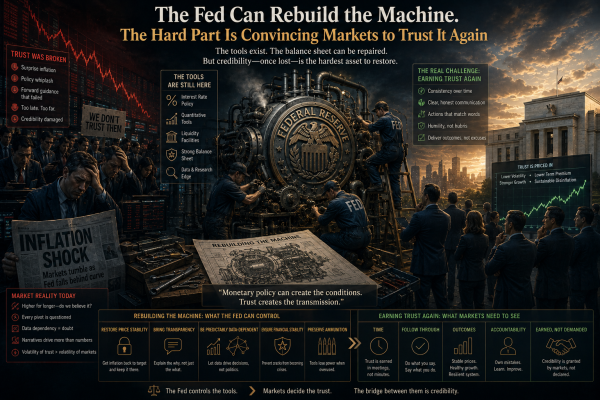

What people often miss is that the system from roughly 2009 through 2021 only worked because several unusually specific conditions existed simultaneously, and many of those conditions no longer exist in the same form today.

Why the Post-2008 Fed Liquidity System Worked

The post-2008 regime worked partly because inflation stayed dormant while liquidity exploded higher. That was the critical ingredient. Quantitative easing created reserves, but the private sector did not aggressively transmit those reserves into broad inflationary lending or runaway spending. Much of the money remained trapped inside the financial plumbing because regulation after the Global Financial Crisis pushed banks toward safety and reserve accumulation rather than aggressive credit creation.

Basel III, liquidity coverage ratios, stress tests, and stricter capital requirements all encouraged banks to hold enormous quantities of liquid assets instead of expanding risky lending aggressively. The result was strange but stable. The Fed expanded its balance sheet dramatically while inflation remained relatively subdued for years.

That experience changed policymaker psychology completely because it convinced many people that central bank balance-sheet expansion carried fewer consequences than earlier generations feared.

How the Reverse Repo Facility Supported Market Stability

Then came the Reverse Repo Facility, which acted as a kind of overflow valve after the 2020 stimulus surge flooded the system with excess cash. Money-market funds suddenly held enormous quantities of liquidity while short-term collateral yielding anything attractive became scarce. The Fed effectively absorbed that pressure by offering the RRP with administered interest, giving institutions somewhere safe to park excess liquidity rather than forcing it directly into broader speculative channels all at once.

That environment depended on several conditions aligning simultaneously: low inflation, strong global demand for Treasuries, weak loan demand relative to reserves, banks comfortable absorbing duration risk, foreign buyers recycling dollar surpluses into U.S. debt, and very low fiscal interest costs.

Several of those conditions have deteriorated materially.

Why Banks No Longer View Treasury Risk the Same Way

The biggest issue today is not whether the Fed can mechanically create reserves again. It can. The harder problem is balance-sheet tolerance and inflation sensitivity. During the 2010s, banks could hold enormous Treasury positions relatively comfortably because rates sat near zero and long-duration price volatility remained subdued. Once rates exploded higher in 2022, the system rediscovered something many investors had forgotten: long-duration Treasuries can generate enormous unrealized losses very quickly when yields move aggressively upward.

That realization sat at the center of the 2023 regional banking stress.

Suddenly banks no longer viewed duration exposure as a harmless parking place for liquidity. Depositors also became less passive after watching several institutions unravel under pressure. Money moves faster now because digital banking accelerates reactions. The old assumption that deposits would remain sticky during stress weakened materially after 2023.

That changes the equation.

Banks today are far more cautious about absorbing massive duration exposure unless compensation improves significantly. Even if regulators quietly encourage Treasury absorption again, institutions cannot completely ignore mark-to-market risk or liquidity flight concerns. The psychological framework changed after rates repriced violently higher.

Inflation Expectations and the Trust Problem

Inflation creates the second major problem.

From 2009 through 2019, the Fed operated inside an environment shaped by globalization, cheap energy, weak velocity, aging demographics, technological efficiency, and persistent disinflationary pressure. Policymakers gained enormous flexibility because inflation repeatedly refused to accelerate meaningfully despite years of liquidity expansion.

That confidence broke during 2021 and 2022.

Once inflation pushed above 8%, markets stopped assuming balance-sheet expansion was consequence-free. The entire perception of central bank intervention changed because investors suddenly realized that liquidity injections and fiscal expansion could produce inflationary consequences under different structural conditions.

That is the trap policymakers now face.

The Fed can print reserves indefinitely. What it cannot fully control is how bond markets interpret long-term inflation credibility once deficits remain structurally large and monetary accommodation expands simultaneously. If markets begin interpreting central-bank support less as temporary stabilization and more as fiscal dominance, long-duration yields can rise rather than fall because investors demand compensation for inflation risk and currency debasement risk.

This is why the current environment feels unstable underneath the surface even when headline conditions appear manageable.

Why the United States Is Not Japan

Many analysts point to Japan as the counterexample, arguing that central banks can monetize debt almost indefinitely without severe consequences. But Japan operated under very different structural conditions: persistent deflationary pressure, massive domestic savings pools, home-biased investors, and different demographic and financing structures. The United States depends far more heavily on foreign capital flows and market-based financing mechanisms.

Reserves, Collateral, and the Limits of Rebuilding the System

There is also an important distinction between reserves and usable collateral that often gets ignored in simplified discussions of QE and the RRP system.

The Reverse Repo Facility was never merely “money storage.” It functioned as part of the broader collateral plumbing connecting Treasury bills, repo markets, dealer balance sheets, money-market flows, and short-term funding structures together. Rebuilding a multi-trillion-dollar RRP system would likely require another enormous reserve injection, another collateral shortage, or another major fiscal transfer wave flooding money markets with excess liquidity.

Operationally possible? Certainly.

Stable over long periods? That becomes far less clear.

Treasury Issuance, Debt Absorption, and Market Psychology

Another issue hiding underneath all of this is Treasury issuance itself. During the 2010s, central-bank intervention suppressed volatility partly because private credit demand remained relatively restrained while deficits looked manageable relative to current conditions. Today Treasury issuance remains enormous even during periods nominally described as economically stable.

That means absorption requirements continue growing structurally larger.

At some point the system requires one or more groups to absorb increasing debt issuance: private investors, foreign buyers, banks, or increasingly the central bank itself. The more the final category dominates, the more markets begin questioning inflation credibility, fiscal sustainability, and currency stability over longer horizons.

That does not automatically imply hyperinflation or collapse. People rush far too quickly into extreme language because extremes attract attention. The more realistic concern is that term premiums and long-duration yields may behave very differently than they did during the QE decade because inflation psychology itself has changed.

And psychology matters more than people realize.

The Real Challenge: Rebuilding Trust in the Fed Liquidity System

The old regime functioned partly because markets trusted policymakers, trusted disinflation, trusted globalization, and trusted that liquidity expansion could remain largely trapped inside financial channels without spilling aggressively into broader inflationary dynamics. That trust weakened materially after 2021.

So yes, policymakers can absolutely attempt to rebuild some version of the old reservoir system. Mechanically, they know exactly how to do it.

The more difficult question is whether markets, banks, foreign capital flows, and inflation expectations would cooperate the same way this time around.

That answer remains far less certain, and uncertainty itself is what keeps the current environment feeling unstable beneath the surface, even when the machinery still appears intact.