The Financial Abyss: When Herd Mentality Destroys Wealth

Apr 8, 2025

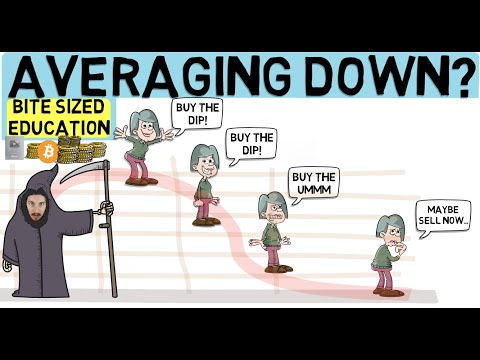

The market doesn’t care about your feelings. While crowds flee burning buildings in panic, they rush into burning markets with equal abandon. This paradoxical human behavior creates the most dangerous financial trap known to investors: the collective delusion that what everyone believes must be true. When stocks plummet, the untrained mind sees only falling knives, while the disciplined investor recognizes potential diamonds scattered amid the wreckage. This precise moment—when fear paralyzes rational thought—creates the fertile ground where averaging down stocks becomes not just viable but potentially transformative.

Markets don’t reflect reality; they reflect perception. And perception, unlike gravity or thermodynamics, follows no natural laws. It warps, distorts, and occasionally shatters under extreme pressure. The 2008 financial crisis wasn’t merely an economic collapse—it was a collective psychological fracture, where even blue-chip companies with rock-solid fundamentals traded at absurd discounts to intrinsic value. Those who averaged down stocks during this period, methodically and selectively, later found themselves sitting atop mountains of wealth while others remained trapped in paralysis, waiting for “certainty” that never arrives.

The averaging down strategy represents a direct rebellion against our hardwired instincts. Every neural pathway screams to run when assets decline, yet the mathematical reality remains stubbornly consistent: lowering your average cost basis improves potential returns when recovery occurs. This isn’t blind optimism; it’s calculated probability—a wager placed not on market sentiment but on fundamental business resilience.

The Quantum Nature of Price: Why Averaging Down Stocks Defies Intuition

Consider stock prices as existing in quantum states rather than fixed positions. The observed price represents merely one probability wave collapse, not an objective reality. When we discuss averaging down stocks, we’re essentially exploiting the gap between observed price (the market’s emotional reaction) and unobserved value (the company’s actual worth). This conceptual framework transforms averaging down from a desperate “doubling down” into a sophisticated arbitrage between emotional overreaction and fundamental reality.

Market extremes create nonlinear opportunities. A 50% price decline doesn’t represent a symmetrical risk-reward scenario—it creates an asymmetric upside potential. When a $100 stock falls to $50, it requires a 100% gain to return to previous levels. This mathematical reality means averaging down stocks provides exponentially greater upside leverage the further prices fall from fundamental value. The gravitational pull toward intrinsic worth becomes stronger precisely when fear reaches maximum intensity.

In 2020, when pandemic panic sent markets into free-fall, Warren Buffett’s apparent inaction confused many observers. Yet beneath this seeming passivity lay a profound understanding: price declines create opportunities only when matched with business quality. Averaging down stocks works not as a universal principle but as a targeted weapon deployed with surgical precision. The strategy demands both courage and discrimination—two qualities perpetually in short supply during market dislocations.

When the Abyss Stares Back: Distinguishing Value Traps from Temporary Dislocations

Not all declining assets deserve additional capital. The most dangerous phrase in investing—”it’s so cheap now”—has led countless investors into value traps where averaging down stocks becomes a pathway to financial ruin. The distinction lies not in price movement but in underlying business resilience. Kodak appeared “cheap” for years during its decline, while Apple at $27 post-2008 crisis seemed “expensive” to many observers fixed on backward-looking metrics.

The key questions when averaging down stocks must focus on antifragility: Does this business become stronger through market stress? Does it possess adaptive capacity? Would its competitive position improve if conditions worsened? Nassim Taleb’s concept of antifragility provides the perfect lens for evaluating averaging down candidates—seeking not merely businesses that survive chaos but those that potentially thrive from it.

Averaging down stocks requires distinguishing between cyclical downturns and secular declines. The former creates magnificent wealth-building opportunities; the latter ensures permanent capital destruction. The oil industry during 2020 demonstrated this distinction perfectly. While integrated majors with diverse energy portfolios represented potential averaging down candidates, pure-play shale producers facing structural challenges often became financial graveyards for additional capital.

The discipline to average down stocks requires psychological immunity to both external noise and internal doubt. When markets convulse, information quality deteriorates precisely when its value increases. Media narratives amplify rather than analyze, creating additional layers of distortion. The contrarian investor must therefore maintain an information edge—not through faster news consumption but through superior analytical frameworks that cut through emotional static.

Mathematical Precision: The Calculus of Averaging Down

Averaging down stocks isn’t merely psychological courage—it’s mathematical precision. Consider an initial position of 100 shares purchased at $50, representing a $5,000 investment. If the stock declines to $25 and you purchase an additional 100 shares, your average cost basis becomes $37.50. A recovery to just $40 would still generate profit, despite remaining 20% below your initial entry price.

This mathematical advantage becomes more pronounced with each incremental decline, creating a powerful compounding effect when recovery occurs. Unlike gambling, where each wager stands independent of previous results, averaging down stocks creates an integrated position where new capital directly enhances the profile of existing capital. It transforms past “mistakes” into future opportunities—provided the underlying business fundamentals remain intact.

Position sizing becomes the critical variable when averaging down stocks. The traditional “equal weighting” approach often proves suboptimal compared to dynamic position sizing based on differential between price and value. Jesse Livermore’s methods, often misunderstood as pure technical speculation, actually incorporated brilliant position sizing during market dislocations. His approach of increasing position size as confidence grew—rather than frontloading risk—provides a template for modern averaging down strategies.

The averaging down stocks approach must incorporate time as an explicit variable. Capital deployed must align with expected recovery timeframes, requiring liquidity management that matches position horizons. Too many investors destroy otherwise sound averaging down strategies by deploying capital needed for near-term obligations, forcing liquidation precisely when patience would yield rewards.

The Psychological Battlefield: Overcoming Your Greatest Enemy

Averaging down stocks represents not merely a financial strategy but a direct confrontation with your psychological limitations. The market creates perfect pain points—declining just enough to maximize doubt before recovery begins. This phenomenon isn’t coincidental but emerges from collective psychology where maximum fear precedes inflection points. The successful practitioner of averaging down stocks must, therefore, develop almost inhuman emotional discipline.

The biological realities cannot be ignored. Under stress, blood literally flows away from your prefrontal cortex—the decision-making center—toward limbic regions controlling fight-flight responses. This physiological reality means that averaging down stocks must be executed through pre-commitment strategies established during periods of calm reflection. The heat of market panic is precisely when your decision-making capacity reaches its nadir.

Charlie Munger‘s approach provides the antidote: inversion thinking. Rather than asking, “Should I buy more?” when stocks decline, ask “What would cause me to never want this business at any price?” This inversion creates psychological distance from immediate price action, redirecting focus to business fundamentals where averaging down stocks becomes a rational rather than emotional decision.

The averaging down stocks strategy requires maintaining two contradictory thoughts simultaneously: acknowledging that markets may continue declining indefinitely while maintaining conviction that fundamental value will eventually prevail. This cognitive dissonance proves unbearable for most investors, which precisely explains the strategy’s effectiveness. If it were psychologically easy, the opportunity would disappear through widespread adoption.

Tactical Deployment: Leveraging Options for Enhanced Averaging Down

Advanced practitioners can amplify averaging down stocks through options strategies that convert market volatility into direct income. When fear spikes, option premiums expand exponentially, creating opportunities to sell puts at strike prices where you’d gladly purchase shares. This approach transforms averaging down from passive reaction to proactive opportunity creation.

Consider a stock trading at $40 that you’d eagerly acquire at $30. Rather than placing limit orders, selling cash-secured puts at the $30 strike generates immediate premium income while creating the opportunity to purchase shares at an effective price even lower than your target. This approach to averaging down stocks converts market anxiety directly into tangible cash flow while establishing positions at advantageous prices.

For existing positions facing decline, covered call strategies can reduce basis while generating income during sideways consolidation periods. This creates a three-dimensional approach to averaging down stocks: additional share purchases at lower prices, premium income from strategic option sales, and dividend capture for income-generating securities. Together, these vectors create a powerful cost-basis reduction system that accelerates potential recovery.

The most sophisticated averaging down stocks approach incorporates correlation analysis across your entire portfolio. Strategic averaging should increase, not compound, existing exposures. This means deliberately seeking negative correlation within averaging candidates—businesses that would respond differently to various economic scenarios. This prevents the catastrophic risk concentration that destroys many otherwise sound averaging strategies.

The Ultimate Test: Conviction Amid Chaos

Averaging down stocks reveals character more than intelligence. Many investors intellectually understand the mathematics but emotionally crumble when theory meets reality. The strategy demands not merely understanding but embodiment—the ability to act with conviction precisely when conviction seems foolish. This represents the ultimate arbitrage opportunity: exploiting the gap between what humans know and what they can actually execute under pressure.

The most powerful examples of averaging down stocks come not from academic theory but from lived experience. During March 2020, when markets collapsed amid pandemic uncertainty, quality businesses across sectors traded at multi-year lows despite having balance sheets capable of surviving prolonged disruption. Those who systematically averaged down during this period didn’t merely recover losses but often generated multi-year returns in months—not through speculation but through mechanical execution when others froze.

The averaging down stocks strategy ultimately reveals a profound truth about markets: they’re less efficiency mechanisms than emotional amplifiers, swinging between extremes of fear and greed with only occasional visits to rationality. The disciplined investor exploits these emotional oscillations not through prediction but through preparation—establishing systems that activate precisely when human judgment typically fails.

For those with both the temperament and analytical framework to execute properly, averaging down stocks represents perhaps the single most powerful wealth-building strategy available to individual investors. It transforms market chaos from threat to opportunity, converting temporary price dislocations into permanent wealth accumulation. In a financial landscape increasingly dominated by algorithmic trading and institutional money flows, the ability to average down with discipline may represent the last sustainable edge available to the individual investor willing to stand apart from the herd.