Extracted from the August 26, 2011, Market Update

Not A Good Time To Buy Gold Bullion

We have repeatedly stated that when it comes to Gold and precious metals, in general, our goal is to only wait for our indicators to move into the oversold to extremely oversold ranges before we start deploying fresh money into this sector. However if in the process of waiting for these developments Gold and Silver experience adamant pullbacks we will view that as a bonus. Having said that there is absolutely nothing that states that Gold will not potentially experience a sharp pullback; many commodities have already experienced what could be termed as back-breaking corrections. Thus it would seem unlikely that Gold is going to be completely spared this fate. Interestingly we have some data that indicates all is not well in the Gold market.

Recent 2017 article that you might find interesting: Should you fear Stock Market Crashes

According to the World Gold Council, the largest buyers of Gold, year over year for the second quarter of 2011 were the following four countries.

| Market | Demand |

| India | +38% |

| China | +25% |

| U.S.A | -22% |

| Europe | -48% |

Immediately, one can see that the largest buyer is India followed by China. The U.S. and Europe have dramatically cut back on Gold purchases. At this point in time, it appears that its India and China that are supporting the Gold market. What happens if for some reason these chaps cut back on their purchases, it could adversely affect the price of Gold. Granted times are bad in the US and Europe, but growth in China is stalling, and if the Chinese economy experiences a pullback it won’t be long before it hits the rest of Asia. Demand in the US dropped by 22% and by a whopping 48% in Europe. One minute demand was huge in both these zones and the next minute things changed.

Gold Stock Market Crash could become a reality

There is one outside factor that needs to be considered. If India experiences a good monsoon season, then farmers will be flush with cash as a good monsoon season means good harvests. Indian farmers plough a significant portion of their money into Gold. Thus there is a chance that demand for Gold could surge at least in India, but this could be balanced with further declines in the US and Europe; the Chinese might also cut back if the economy starts to cool off there. Given the current set up it would not be wise to Buy Gold Bullion at this time. General Equities make for a much better investment.

Glaring Discrepancy that could be the trigger for Gold stock Market Crash

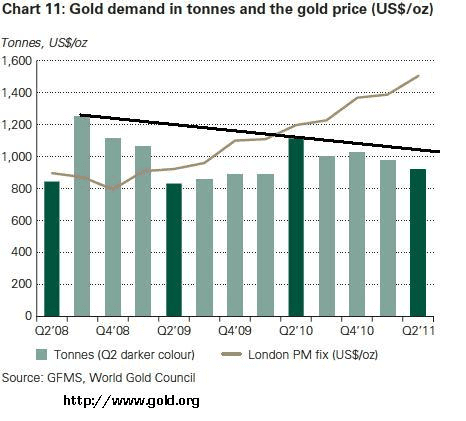

The total global supply of Gold dropped 4% year over year to roughly 1,060 tonnes at the end of the 2nd quarter according to the World Gold Council. However, demand for Gold (Jewellery, ETF’s, technology, dentistry, Gold bars, coins, etc. ) fell to 919.8 tonnes in the 2nd quarter; that is a large drop of 17% year over year.

Investment demand dropped 37, and most of this was driven by ETF’s. Not too long ago ETF’s were one of the largest buyers of bullion, so this big drop is rather troubling at least in the intermediate time frames.

The price of Gold is rising while supplies are also rising; this is not the norm, something is totally out of whack here. Prices climb when supplies drop and not the other way around. Such anomalies never last and usually tend to end badly; it’s just a question of time. The longer such anomalies last, the more painful the ensuing correction is likely to be.

The chart below illustrates clearly illustrates this distorted relationship.

One could state that from the 4th quarter of 2008 demand has started to drop; we had a few spikes here and there (one in Q2 2010, and smaller ones in Q4 2010), but in general, if you look at the trend line you can see that it’s headed downwards.

Demand governs price, and when this relationship goes out of balance (as it is right now), then something is not quite right. It’s pretty much similar to the market moving higher and higher on lower and lower volume. This move up is akin to what the market has done; it moved higher and higher on lower and lower volume, and then look how fast the situation suddenly changed. Gold has been trending higher and higher on lower and lower demand; demand is analogous to volume in the market because they both represent buyers.

Masses are Euphoric and this indicates Gold Markets are ripe for A crash

So many people have piled into Gold ETF’s that if there were a sudden rush for the exits these ETF’s would be forced to potentially unload large amounts of Gold, which could lead to a vicious cycle of selling. Our point here is not to scare anyone. In fact, if this outcome came to pass we would view it as a splendid development, for it would provide traders with a lovely long-term buying opportunity. Our ultimate price target for Gold is still in the $5,000 ranges. And we feel that Silver will at the very minimum trade to the $150-$200 ranges.

Bottom line; it’s not the time to buy Gold now or any precious metal. The only exception might be Silver, and that’s only if you have a long-term horizon; in other words, you have the ability to focus on the long-term time frames and forget what is going on in the short and intermediate time frames. Very few traders have this ability, but once mastered it almost always helps you spot great investment opportunities.

We suspect that Silver could trade down to the $25-$30 ranges before a bottom takes hold. At those prices Silver will make for a good buy; if by some chance it should dip to 20 or below it will become a screaming buy.

Other Interesting Articles

Why market crashes are buying opportunities

Why Mechanical and Technical Analysis Systems Fail

The Limitations of Trend Lines

Contrarian Investment Guidelines

Inductive Versus Deductive reasoning

Portfolio Management Suggestions

The Good And the Ugly On Trading Futures